May 2026 Market Pulse: Expert Q&A on K-Shaped Economic Trends, SMB Risk, and More

Highlights:

- Market Pulse experts analyze the "K-shaped" economic impact, noting that small businesses face twice the downturn risk of large corporations, emphasizing the need for targeted, data-backed financial support.

- Financial institutions can proactively manage portfolio risk by monitoring indicators such as credit utilization spikes, payment velocity shifts, and credit-seeking behaviors to identify early signs of stress.

Both before and during each Market Pulse webinar, our audience submits their burning questions to our expert panelists.

For our May Market Pulse webinar, our panel included Dr. Robert Wescott, President of Wescott Strategic Advisors, Jill Molitor, Director of Fraud and Credit Administration at Stearns Bank, and Jesse Hardin, Senior Advisor at Equifax. Below are their answers on questions around economic trends, the K-shaped economy, credit risk, and more.

Q: You talked about a K-shaped economy for the consumer. Given the NFIB Survey of Small Businesses and top-of-mind issues, isn't there a K-shaped economy for businesses as well?

Dr. Robert Wescott, Wescott Strategic Advisors: So, that's a really smart question, and many of those in e-commerce is asking that exact same question, even in the last couple of months.

Yes, there is a bit of a K-curve effect for small businesses, and let me just start by saying there's a K-curve between smaller businesses and larger businesses. We've done a lot of analysis on that. In a normal economic downturn, small businesses have, essentially, twice the impact of large businesses. Big businesses, like household brands, have deep pockets and capital bases. They might not lay people off, but smaller businesses do.

Secondly, if there is an economic downturn, and that's when most of the stress would build up in a small business sector, it really depends on what you are selling and whether there is inelastic demand for it in an economic downturn. You want to sell something that there's inelastic demand for during an economic downturn. Think of products like food, drugstore items, cellphones, and other goods and services. People need their cell phones and they are not going to cancel them in a downturn. Those kinds of businesses would do well, but there are other types of small businesses that may be more optional, such as yoga studios and jewelry stores. They tend to have much more amplitude and would likely suffer more in an economic downturn.

Q: What innovative cashflow solutions, including credit products, should financial institutions consider for small businesses in this economy?

Jill Molitor, Stearns Bank: Your institution's risk appetite, loan policies, and underwriting procedures coupled with the transaction size, loan type, and collateral type should be considered when determining the depth of the financial review coupled with the credit products leveraged.

If the question is geared toward 'application only' flow business, where financials and bank statements are not collected up to a certain dollar threshold, it’s best to leverage commercial solutions from Equifax, which can include both commercial and consumer data, to help determine business size + historical repayment of debt. Take into consideration items such as debt stacking; time in business; industry; transaction size, whether the equipment is replacement or additional.

If the collateral is additional or an 'upgrade,' consider whether they have written contracts to support the additional purchase. There are tools available that, with customer consent, can securely retrieve bank statements from the customer's bank via API, making it seamless for the customer. For larger loans or for loans with required financial statement review (such as a SBA loan), there are spreading solutions available from vendors and many have different levels of automation to summarize data to include an initial credit memo. For proactive portfolio analysis on an individual and a loan portfolio perspective, AbsolutePD® from Equifax is a good tool, and can be leveraged along with internal financial institution data to create even more lift – helping to identify potential defaults before they default, allowing time to reach out to the borrower and talk through potential solutions.

Remember – with ALL solutions utilized, trust but verify. We can outsource the task and can automate the task, but not the accountability of its output.

Q: What is your outlook on which industries are likely to see growth or slowdown, especially looking at default levels?

Jesse Hardin, Equifax: I would refer back to the Equifax absolute probability default model. And when we look at that data, which is gonna forecast out to 2027, we can see that defaults overall are ticking upwards about 3.5% from 2026 to 2027. In sectors like accommodation, food, transportation, and healthcare, they are likely to fare a lot better, while education, mining, information, and other similar sectors are expected to see a bit of a worsening picture. In general, it is probably still a tough, competitive environment. But I think those are some of the sectors where we would think to see some growth or decline.

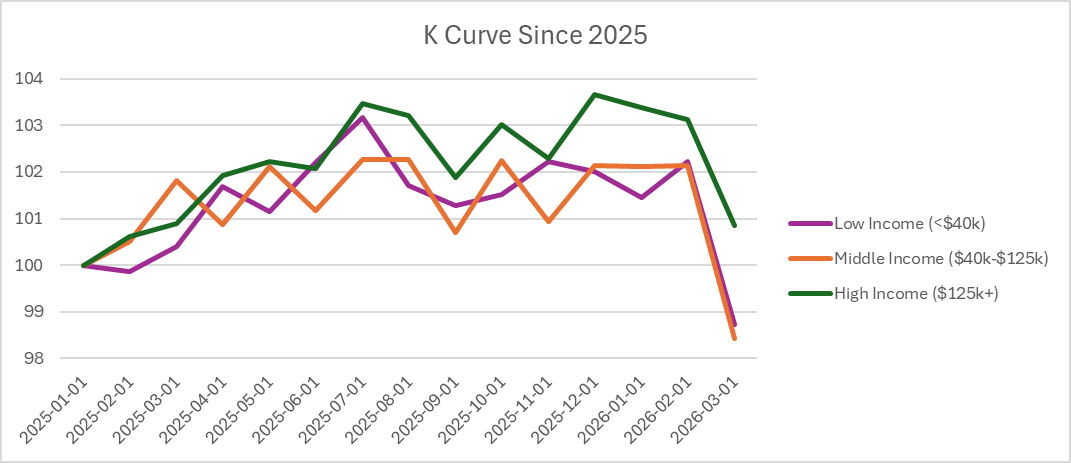

Q: On the K-shaped spending trend: The NY Fed charts index spending growth to January 2023, but it looks like the K-shape started forming in early 2023—then has mostly remained unchanged over the past year or so. Is it possible that consumer spending growth has started to reconverge? If the chart was indexed to Jan 2025, would it still show a K-shape?

Wescott: The K-Curve spending trend is a bit less pronounced when you look at the change since 2025 compared to the change since 2023, but the data suggests that the K-Curve is continuing. As of March 2026, the only income group to show higher spending compared to January 2025 is the highest-income consumers. Throughout 2026, the high-income category has seen consistently higher real growth than both the low- and middle-income groups.

The biggest difference between looking at the data indexed

to 2023 and to 2025 is that the difference between low and

middle-income spending growth has disappeared, meaning that

middle-income consumers appear to be doing worse off compared to

2025 than to 2023.

Q: Are there any variables that can help predict FICO

migration, even directionally?

Hardin: The first one would be credit utilization spikes. If revolving balances are suddenly jumping, that’s gonna have an impact on scores and there may potentially be a score drop.

Another factor would be payment velocity as you could see a shift in payment from pay full statement balances to making minimum payments. That could signal stress and cash flow.

The third variable that comes to mind is sudden credit-seeking behavior, meaning a cluster of hard inquiries in a short window. That may indicate a need for more liquidity and could be an early sign that you may see a movement in score.

Q: I've been hearing about the national debt my whole life...does it affect SMBs in any way?

Wescott: Unfortunately, rising levels of the national debt can have implications for small businesses, and they are negative. We had pretty much forgotten about the national debt over the past 25 years, but it remains a lurking problem. With the budget surpluses of the late 1990s the national debt got down to just 37% of GDP in 2000, but it has soared to over 100% of GDP today. This rising debt burden has been driven by costs associated with the wars in Iraq and Afghanistan, stimulus packages in response to the Great Financial Crisis of 2008 and 2009 and the COVID-19 pandemic, and a persistent political disagreement in the federal government around taxes and spending.

To date, there is no panic in debt markets, but more investors are getting nervous about rising debt levels. If confidence ebbs, which history teaches is likely at some point, long-term interest rates could rise rapidly. For example, in 2022 when short-lived UK Prime Minister Liz Truss announced a budget with tax cuts that spooked UK investors, UK interest rates jumped by 100 basis points in just one day. Small businesses generally have less ability to absorb a sharp increase in interest rates than large businesses, so a slow or rapid increase in interest rates could be expected to hurt small businesses a lot.

Recommended for you