February 2026 Consumer Pulse: The Latest Consumer Credit Trends

Highlights:

-

Outstanding consumer debt continues to climb across mortgage, revolving, and non-revolving categories, while consumer originations generally rose year-over-year through October 2025, indicating continued demand for credit products.

-

Delinquencies present a mixed picture: Bankcard, private label, and personal loan delinquencies improved year-over-year in December 2025, while mortgage and auto delinquencies increased.

The February Market Pulse webinar showcased insights from Equifax Senior Advisor Tom O’Neill around current consumer credit trends.

February 2026 Key Insights: Today’s Consumer Credit Trends

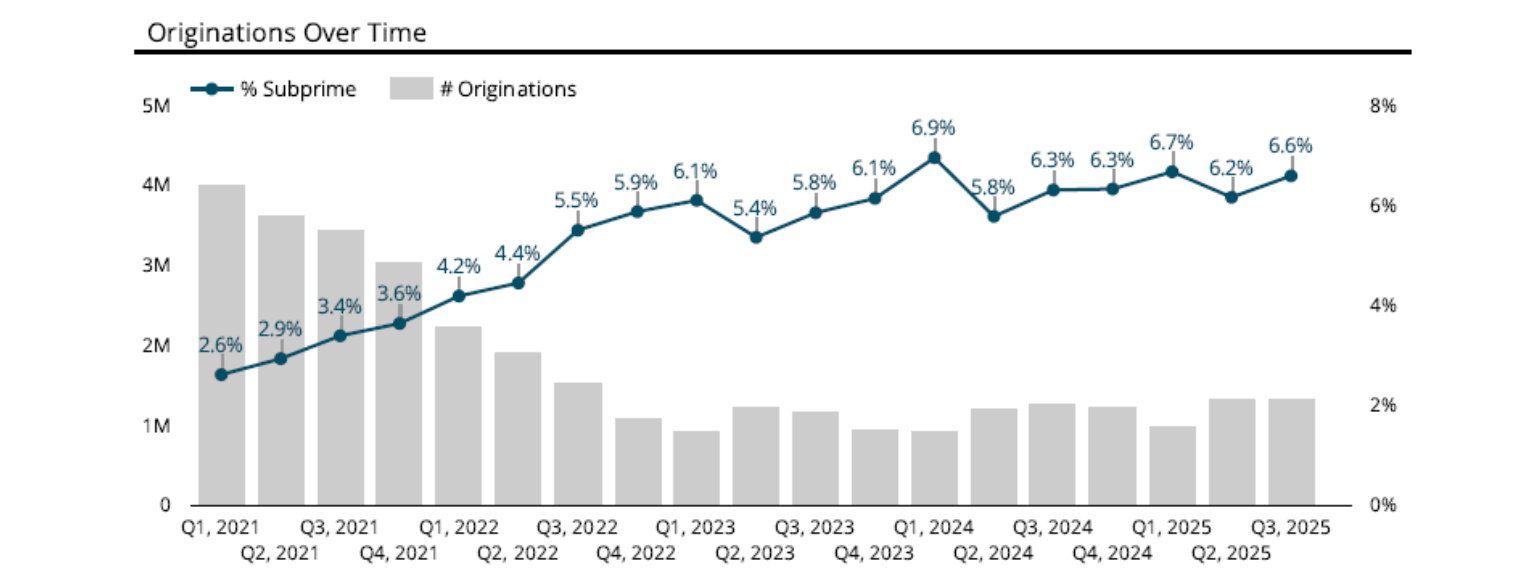

Through October 2025, consumer originations rose

year-over-year across all lending categories, but Private Label Card

was lower year-over-year.¹

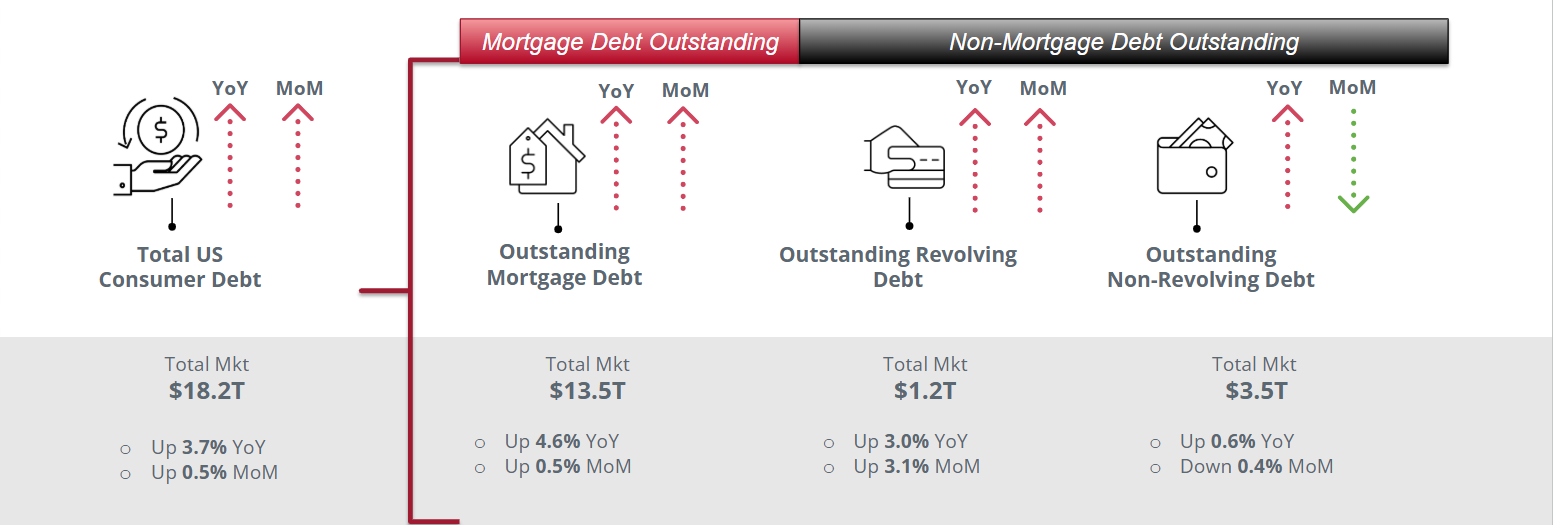

As of December 2025, outstanding mortgage (including first

mortgages, HELOCs, and HELOANs), revolving (including bankcard,

private label cards, and other revolving products), and total

non-revolving consumer debt (including auto loans and leases, student

loans, and personal loans) continue to climb year-over-year.²

As of December 2025, non-mortgage consumer debt outstanding

has increased for auto, bankcards and personal loans year-over-year.

Student loans and private label cards continue to be lower.²

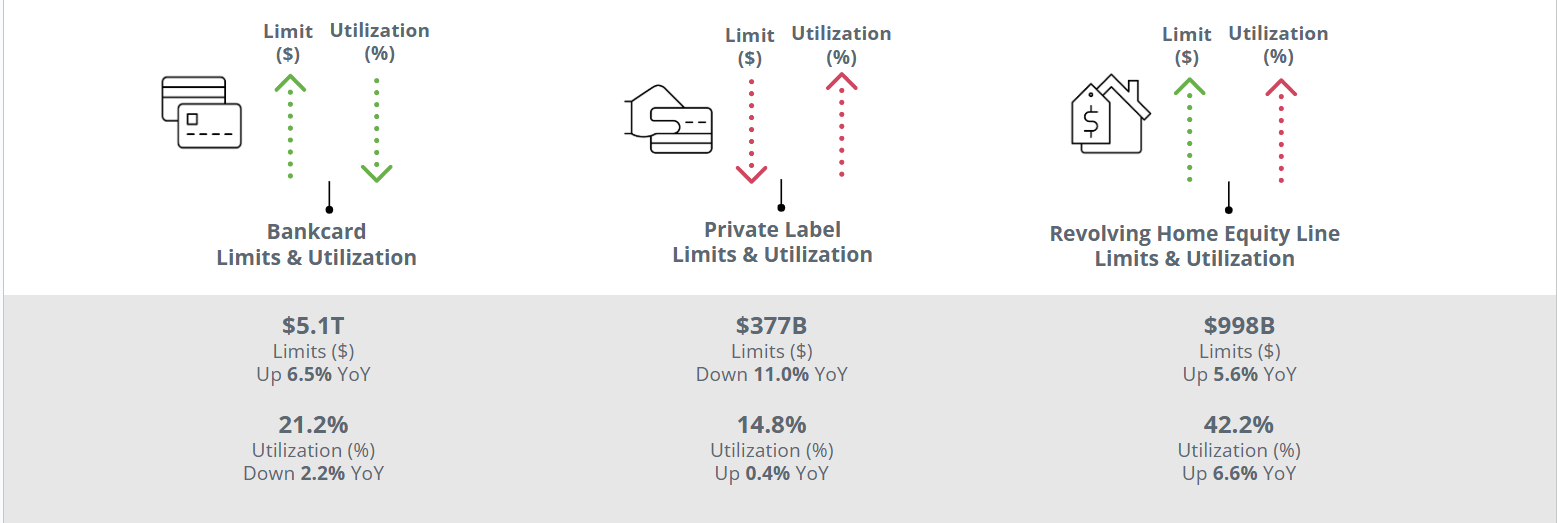

December 2025 saw utilization decrease slightly for bankcard

while credit limit for bankcard increased. Home equity metrics

continue to increase, while private label card metrics are

mixed.²

December 2025 bankcard, private label, and personal loan

delinquencies improved year-over-year, while mortgage and auto

increased year-over-year.²

January 2026 Key Insights: Today’s Mortgage Industry Trends

The rebound in mortgage origination volume has been more of

a “slow thaw” rather than a “spring melt,” with volume improving

gradually. As of October 2025, over 4.1 million accounts and a

corresponding $1.5 trillion have been originated year-to-date, an

increase of over 6.6% and over 12% year-over-year respectively.³

Where are mortgage originations happening? The average buyer is shifting. The share of first-time home buyers is at a historically low level of 21% while the median age of first-time home buyers is at an all-time high of 40 years old, up 7 years from the median age in 2020.⁴

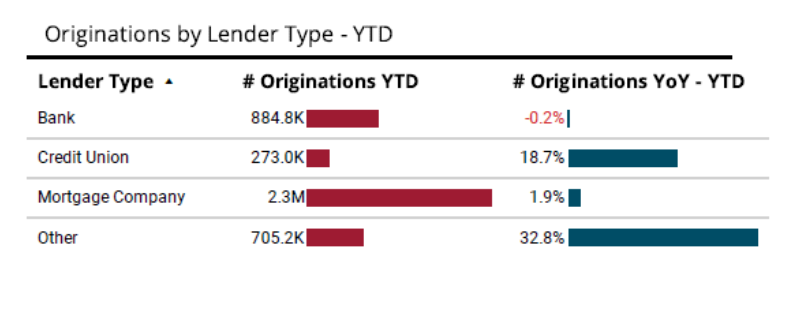

The average lender is shifting a bit as well. As banks see a

slight dip, a decline of .2%, in mortgage originations

year-over-year, credit unions and other lenders have seen

significant year-over-year increases in origination volume.

Traditional mortgage companies are showing a modest increase

year-over-year in volume.³

Keep Your Business Goals Within Sight

Find our monthly Small Business Insights, National Consumer Credit Trends reports, the Market Pulse podcast, and more at our Market Pulse hub.

Broaden your perspective with insights that inspire bold innovation, confident adaptation, and decisive leadership through Trend and Insights.

Sources:

-

Equifax US National Consumer Credit Trends Originations Report from January 2026 - Data through October 2025

-

Equifax US National Consumer Credit Trends Portfolio Report from January 2026 - Data as of December 2025

-

Equifax Mortgage Insights Report from February 2026 - Data as of October 2025

-

National Association of Realtors, 2025 Profile of Home Buyers and Sellers

(c) Equifax Inc. 2025. All Rights Reserved. The statistics provided herein are for informational and illustrative purposes only and shall not be used for any other purpose.

*The opinions, estimates, and forecasts presented herein are for general information use only. This material is based upon information that we consider to be reliable, but we do not represent that it is accurate or complete. No person should consider distribution of this material as making any representation or warranty with respect to such material and should not rely upon it as such. Equifax does not assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice. The opinions, estimates, forecasts, and other views published herein represent the views of the presenters as of the date indicated and do not necessarily represent the views of Equifax or its management.

Recommended for you