Legacy and Stability: Why Baby Boomers and Traditionalists Remain the Gold Standard for Financial Security

Highlights:

-

Baby Boomers and Traditionalists maintain the highest financial stability in the market, benefiting from asset-backed resilience that insulates them from K-shaped economic volatility.

-

As the "Great Wealth Transfer" approaches, lenders and retailers must leverage these low-risk, asset-rich consumers while building multi-generational engagement strategies to capture shifting capital.

Welcome to the third installment of our four-part blog series exploring the unique financial realities and trends of four different generational groups (millennials, Gen Z, Gen X, and baby boomers & traditionalists) in the U.S. In each blog, we will take a deep dive into the consumer, credit, and wealth perspectives of these groups to provide lenders and retailers with actionable insights for today's market.

In our first post, we explored why one-size-fits-all strategies fail millennials in today’s K-shaped economy, and in our second installment, we turned our attention to Gen Z, the digital-first generation with the most momentum in the current k-shaped economy. In the third blog of the series, we examined Gen X, the generation facing some of the greatest pressure in the current economic environment. Today, we close the series by looking at the two most stable generations: baby boomers and traditionalists.

Born between 1928 and 1945, traditionalists, also known as the Silent Generation, grew up in the aftermath of the Great Depression and World War II, eras known for financial austerity. This is a sharp contrast from the childhoods of baby boomers, the following generation born between 1946 and 1964, which is mostly characterized by the thriving postwar economy of the 1950s and 1960s. Retired or nearing retirement, many members of these generations are experiencing unparalleled financial stability, even in today’s K-shaped economy, due to their assets protecting them from financial volatility.

Leading the Pack in Market Stability

Data from the Q4 2025 Market Pulse Index Report indicates that every age group experienced a slight dip in their index averages this quarter, representing their first shared decline in two years.

While the average Market Pulse Index for the U.S. population remained at 61.6, baby boomers and traditionalists continue to hold the highest levels of financial stability across all age groups:

-

Baby boomers registered a Q4 2025 Market Pulse Index of 64.5. This marks a year-over-year increase of 0.46% and stands as the highest Market Pulse Index of any generation.

-

Traditionalists followed closely with a Q4 2025 Market Pulse Index of 61.6. This represents a year-over-year increase of 0.22%, securing the second-highest index of any generation.

From Q2 2023 to Q4 2025, the number of these households reaching the highest stability tier (Market Pulse Index of 80+) expanded by 24%. In that same window, the middle stability tier (Market Pulse Index of 50-79) decreased by 5%, and the lowest stability tier (Market Pulse Index of 49 and below) increased by 7%. Notably, these shifts, a 5% decline in the middle tier and a 7% rise in the lowest tier, represent the smallest reduction of the middle tier and the smallest increase of the lowest tier observed across any generation, demonstrating the unique resilience of their asset-backed stability.

Declining Shares of Consumer Debt

As older generations prioritize wealth preservation, their overall credit footprint continues to shrink. With the sole exception of Gen Z, the two oldest generations hold some of the lowest shares of total U.S. consumer debt, and those shares are still declining.

-

As of January 2026, baby boomers held 20.5% of total U.S. consumer debt, which is down 9.8% from January 2020.

-

As of January 2026, traditionalists held just 2% of the total debt, reflecting a 2.5% decrease from January 2020.

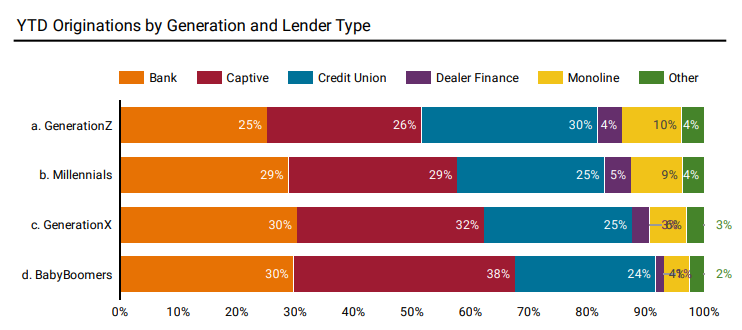

Lender Preferences in the Auto Market: A Traditional Approach

When navigating major purchases like vehicles, baby boomers

express clear preferences for traditional financing institutions.

According to the April

2026 Market Pulse Automotive Insights Report, baby boomers

heavily favor more traditional lenders over newer alternatives. They

demonstrate the highest preference for captive lenders of any

generation, and they tie with Gen X for the highest preference for

banks. Conversely, baby boomers show the least preference for dealer

finance, monoline lenders, and other alternative lender types compared

to all other generations.

The Horizon: Looking Ahead to the “Great Wealth Transfer

While these generations currently hold a dominant financial position, a significant decline in their total assets is anticipated in the near future. The financial landscape is standing on the precipice of the "Great Wealth Transfer," which is slated to be the largest intergenerational hand-off of capital in human history.

As baby boomers and traditionalists pass down their legacies, they are estimated to transfer roughly $84 trillion in personal U.S. assets to Gen X and Millennials through the year 2045. This massive movement of capital is poised to fundamentally reshape the broader financial environment as wealth transitions to the next generations.

What This Means for Lenders and Retailers

Understanding the financial behaviors and immense capital shifting within these two oldest generations is critical for businesses looking to engage them effectively. Here are three key actionable takeaways for lenders and retailers:

-

Optimize for Traditional Auto Financing Preferences: Baby boomers exhibit a distinct preference for conventional auto lending structures, holding the highest preference for captive lenders of any generation and tying with Gen X for the highest preference for banks. Conversely, they show the lowest affinity for dealer finance, monoline lenders, or alternative financing setups. Lenders looking to capture this demographic's auto business must prioritize clear, direct banking relationships and robust captive finance offers rather than relying on decentralized dealership financing packages.

-

Leverage Low-Risk Profiles for Premium Portfolios: The fact that their asset-backed stability insulated them from the sharper K-shaped declines seen in younger demographics and that they have some of the lowest shares of total U.S. consumer debt of any generation means these consumers represent an incredibly low-risk, highly stable pool for premium financial products, low-leverage refinancing, and wealth preservation services.

-

Proactively Prepare for the $84 Trillion Transition: While these cohorts currently boast the highest financial stability indexes in the market, businesses must recognize that this asset concentration is temporary. With the "Great Wealth Transfer" on the horizon, banks and retailers must build multi-generational engagement strategies. Establishing trust with baby boomers and traditionalists today is the critical first step to retaining those assets as they transition to the next generation of consumers.

Recommended for you