Unlock Growth and Mitigate Risk: Optimizing Consumer Loan Decisions with Data

Highlights:

-

Optimizing consumer loan decisions requires smart, data-driven strategies that adapt to the evolving lending landscape.

-

Beyond traditional credit scores, leveraging historical data, industry insights, and alternative data sources (like telecom or specialty finance data) is crucial for refining risk and pricing tiers.

-

Continuous portfolio monitoring is essential for identifying delinquency risks, managing debt reserves, growing share of wallet, combating synthetic identities, and preventing losses through frequent reviews.

In today's dynamic economic landscape, consumer lending isn't just about providing funds; it's about making smart, data-driven decisions that foster growth and mitigate risk. For lenders, staying competitive means constantly refining your approach to loan applications, pricing, and portfolio management. The good news? The power to do so lies within your data.¹

The Evolving Lending Landscape: Why Data is More Critical Than Ever

The foundation of your lending policy – credit scores – are essential, but their predictive power can shift. Why? Several factors contribute to this fluidity:

-

Economic Cycles & Government Policy: Economic stimulus, payment pauses (like those for student loans in the 2020s), and broad economic shifts directly impact consumers' financial health and, consequently, their ability to repay.

-

Regulatory Changes: New regulations can alter how you assess risk and what data you can consider.

-

Emergence of New Industries: The rise of Buy Now, Pay Later (BNPL), credit builder products, and rental payment reporting introduces new credit behaviors and data points.

-

Shifting Score-to-Non-Payment Odds: A 700 credit score today might carry a different risk profile than it did four years ago. For instance, 90+ DPD rates for 701-720 in Q4 2023 were higher than those for 661-680 four years prior. Are your risk and pricing tiers truly aligned with today's score-to-non-payment odds, especially within your specific geographic footprint and field of membership?

These changes directly affect crucial loan portfolio measures like auto-decision rates, approval rates, loss forecasting, and reserve setting.

Refining Your Risk and Pricing Tiers: A Data-Driven Approach

Optimizing your consumer lending policy starts with a deep dive into your existing data and supplementing it with external insights.

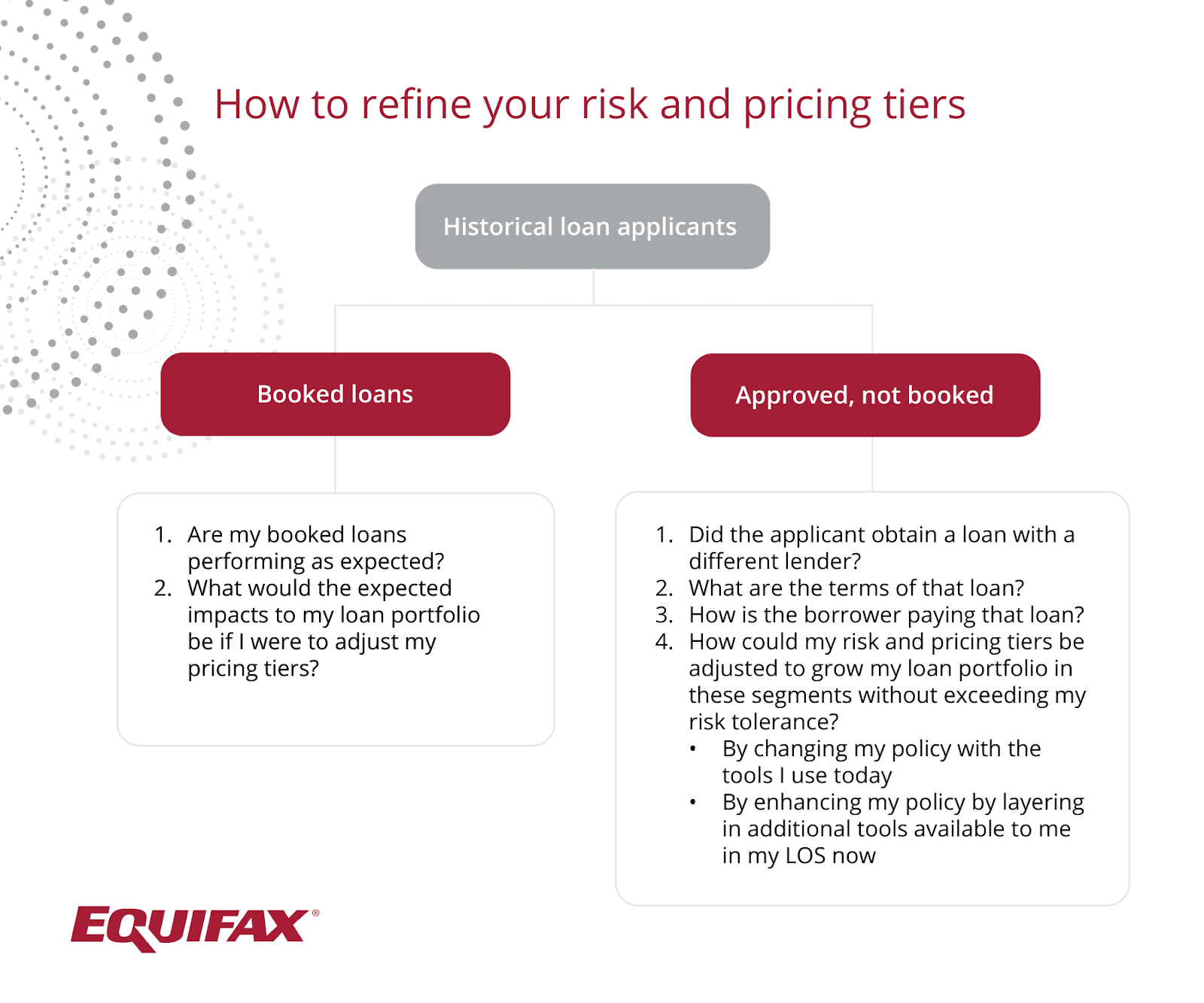

1. Analyze Historical Loan Applicants

Your own historical loan data is a goldmine. When looking to evaluate your lending policy, start the process by looking internally.

Separate previous applicants into three categories: Booked, or applicants that were approved and followed through the loan process with your organization, Approved and Not Booked, meaning applicants that were approved but who ultimately took a loan elsewhere, and Denied. After doing so, ask some questions about the first two groups:

2. Utilize Industry and Peer Data as a Guide

Your historical data, while valuable, may not always be sufficient to confidently make significant decisioning changes. Supplement it with other kinds of industry data to validate your understandings and identify opportunities, such as:

-

Lenders of Similar Size and Industry: Look at how your peers are performing and what their approval and loss rates are for similar segments.

-

Geographic Footprint: Understand the unique lending dynamics in your operational areas.

-

Customer/Member Borrowing Habits: Gain insights into where your customers or members are taking out loans with other providers. This "share of wallet" understanding is critical for strategic growth.

Harnessing the Full Power of Data: Beyond Traditional Credit Scores

To truly optimize, you need to broaden your data horizons.

Traditional credit files offer a robust, but sometimes incomplete, picture. Alternative data sources can illuminate credit behaviors of consumers who are thin-file or credit invisible, meaning without a credit file, or provide additional insights for those with traditional files:

-

Telecom, Pay TV, and Utilities Data: Payment history from over 160 service providers, representing 222 million consumers, with 38 million not found in traditional credit files. This data can reveal responsible payment behavior for essential services.

-

Specialty Finance Data: Payment history from non-traditional banks and lenders, covering over 80 million borrowers, offering insights into a different segment of the lending market.

-

OneScore: A next-generation risk score pairing industry-leading, traditional consumer credit attributes with differentiated alternative data sources — helping score more consumers and enhance decisioning power.

Proactive Portfolio Monitoring: Staying Ahead of Risk

Your data-driven approach shouldn't end at the point of decision. Continuous portfolio monitoring is essential for managing existing risk and identifying new opportunities.

-

Identify Delinquency Risk: Monitor existing accounts to pinpoint customers at high risk of delinquency, enabling proactive intervention.

-

Debt Reserves and Portfolio Mix: Accurately determine the proper level of funding for debt reserves and refine your portfolio credit mix based on real-time insights.

-

Grow Share of Wallet with In Market Solution Suite: Reach consumers actively seeking new credit by providing timely insights by using solutions such as TargetPoint Triggers and TargetPoint Intent Scores. This enables you to deliver targeted offers, increasing customer acquisition and retention.

-

Combat Synthetic Identities: Using solutions like Synthetic ID Alerts can help find and flag suspected accounts opened using synthetic identities within your existing portfolio.

-

Prevent Losses Through Frequent Review: Shifting from annual to quarterly reviews can increase the amount of exposed dollar risk saved by 1.7 times. Moving to monthly reviews can save 6 times more, by allowing lenders to act immediately upon recognizing delinquency with another lender.

By embracing a comprehensive, data-driven strategy across your consumer loan decision process, you can unlock new avenues for growth, enhance profitability, and navigate the evolving lending landscape with confidence. The future of lending is intelligent, informed, and undeniably data-powered.

Source:

-

Blog adapted from talk given by Dave Whitin at MeridianLink Live! 2025 on May 6, 2025 in Orlando, Florida