Don't Get Left Behind: The Urgent Need to Test VantageScore 4.0 Today

Highlights:

-

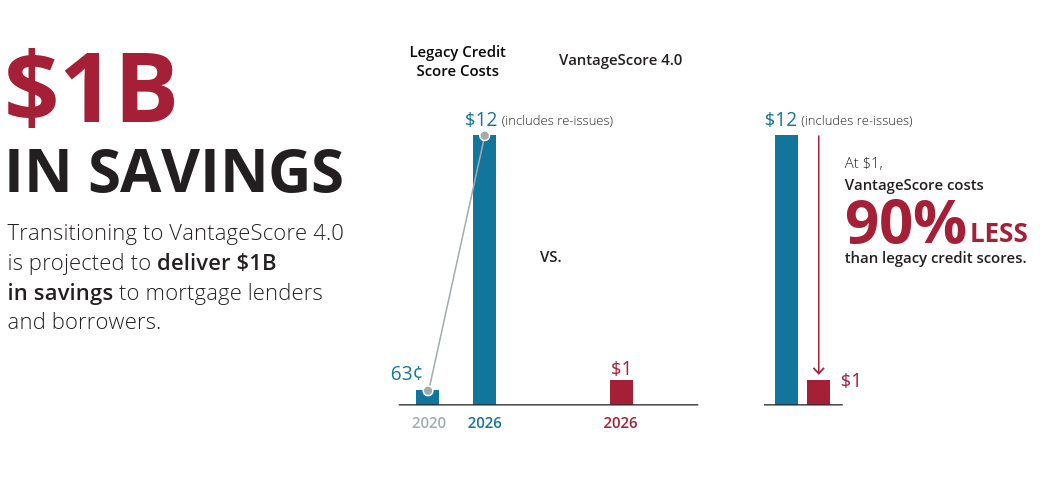

Mortgage lenders risk losing their competitive edge and incurring higher costs by delaying the adoption and testing of the newly approved VantageScore 4.0.

-

Lenders must prioritize testing VantageScore 4.0 now, leveraging loan-by-loan flexibility to understand new, separate pricing structures and capture market share.

The mortgage industry officially entered a new, competitive era of credit scoring following the historic joint announcement by the FHFA and HUD on April 22, 2026. With implementation timelines and eligibility now established for VantageScore 4.0 on mortgage loans sold to the GSEs and FHA, the mandate for lenders is clear: the time to act is right now.

If your institution hasn't started testing and preparing to use VantageScore 4.0, you are already falling behind your competitors.

We are currently in a critical "interim phase" where 21 approved lenders are actively participating in a limited rollout. These early adopters are moving quickly. In fact, approved lenders are immediately permitted to originate and securitize VantageScore 4.0 mortgages through the GSEs, and Freddie Mac has already successfully taken delivery of $10 million in mortgages originated with VantageScore. Additionally, the FHA will soon permit the use of VantageScore 4.0 as an eligible credit scoring model for FHA-insured mortgage underwriting.

In a recent National Mortgage News (NMN) survey of 123

mortgage professionals, 69% of mortgage professionals agree that

adopting a non-legacy credit score offers an immediate and

significant opportunity to lower credit reporting costs. In fact,

over half of respondents warned that delaying the adoption of

VantageScore 4.0 introduces financial risk, primarily through

overpaying for legacy scores and losing pricing power. Lenders who

wait to engage with this transition risk losing their competitive

edge.  Here is why you need to begin testing and preparing your

operational strategy today:

Here is why you need to begin testing and preparing your

operational strategy today:

-

You Have Immediate Flexibility: You do not need to overhaul your entire pipeline overnight. Lenders are granted loan-by-loan flexibility, meaning you are not required to deliver both a Classic FICO and a VantageScore 4.0 score. You can choose which model to use on a per-loan basis (provided the chosen model is consistent for all borrowers on a single loan), making it easier to begin testing on smaller loan populations.

-

Pricing Variations Require Strategy: Classic FICO and VantageScore 4.0 will utilize separate pricing. Commercial terms, including updated Loan-Level Price Adjustments (LLPAs), are available now for approved lenders. Testing VantageScore 4.0 is essential to understanding how these separate pricing structures will impact your bottom line and borrower competitiveness.

There are no initial changes to the GSEs' credit report requirements, meaning you must still obtain scores through a standard tri-merge credit report. The foundational processes remain the same, which removes major friction points for getting started.

Lenders who lean into this implementation, prioritize testing, and engage with their technology partners today will be the ones who capture that new market share. Don't wait until the industry leaves you behind. More information can be found in the GSE Partner Playbook.

Recommended for you