Mortgage Soft Pull Solutions

![]()

Gain A Competitive Edge With Mortgage Soft Pull Credit Reports

Early in the home-buying experience can be a time of anxious uncertainty for borrowers and lenders. But it doesn't have to be.

Soft pull credit solutions help all parties better understand a borrower's foundational creditworthiness on the front-end, prior to underwriting, promoting more confident, seamless, efficient experiences for everyone.

By using mortgage soft pulls that can also deliver income data, trended credit data, and alternative credit data, lenders can better understand more borrowers and the mortgage products that best fit their needs, without impacting borrowers' credit score.

Optimize Mortgage Lending From the Start

A strong mortgage pre-approval process powered by Equifax soft pulls enhances every step of the lending lifecycle:

- Reduced Fallout: Currently, nearly 50% of applicants fall out at the application stage. By moving verification data to the pre-qualification phase, you can filter out unqualified applicants immediately and focus resources on those who will close.

- Frictionless Experience: Borrowers are not required to link bank accounts or provide heavy documentation early in the process. You get the data you need—like tenure and employer name—without adding burden to the applicant.

- Strategic Cost Planning: The Work Number Report Indicator allows lenders to strategically plan for loan origination data needs against cost considerations, avoiding unnecessary report pulls for borrowers who don't have available records.

Save time and costs by pulling full credit files only for borrowers already pre-approved based on soft pulls.

Meet Borrowers Where They Are with Soft Credit Inquiries

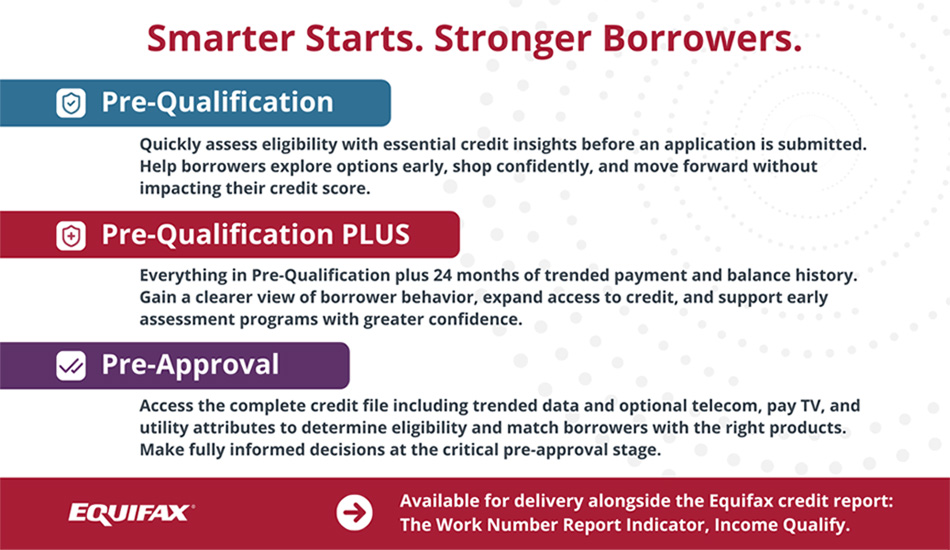

Our soft pull solutions include three distinct options:

Pre-Qualification:

Quickly and efficiently analyze foundational credit information to determine borrower eligibility, pre-application.

- Get a quick preliminary view of mortgage prospects.

- Assist borrowers early without impacting their credit scores.

Pre-Qualification PLUS:

Get all the benefits of Pre-Qualification, plus trended credit data that includes 24 months of payment and balance history.

- Better understand borrower behavior over time.

- Improve access to credit for more borrowers.

- Support GSE early assessment programs.

Pre-Approval:

Unlock the full Equifax credit file including trended data, alternative data for utility and cell phone payments, and the ability to consider verified data in the pre-approval stage.

- Confidently determine borrower eligibility.

- Consult on best-fit mortgage loan products.

- Support GSE early assessment programs.

All three Equifax soft-pull solutions will still require a hard pull with a tri-merge credit report for full mortgage application, loan pricing, final underwriting, and loan closing.

Integrate credit soft pulls early in the lending process so borrowers can confidently shop for homes within their budget sooner, without affecting their credit score.

More Support, Less Friction

Frequently Asked Questions

Related Resources

Related Products

Unlock More Opportunities For Millions of First-Generation Home Buyers

Explore how expanded borrower insights—alternative data such as payment information for cell phones, utilities, and other everyday bills— can be delivered alongside Equifax credit reports.