May 2026 Consumer Pulse: The Latest Consumer Credit Trends

Highlights:

-

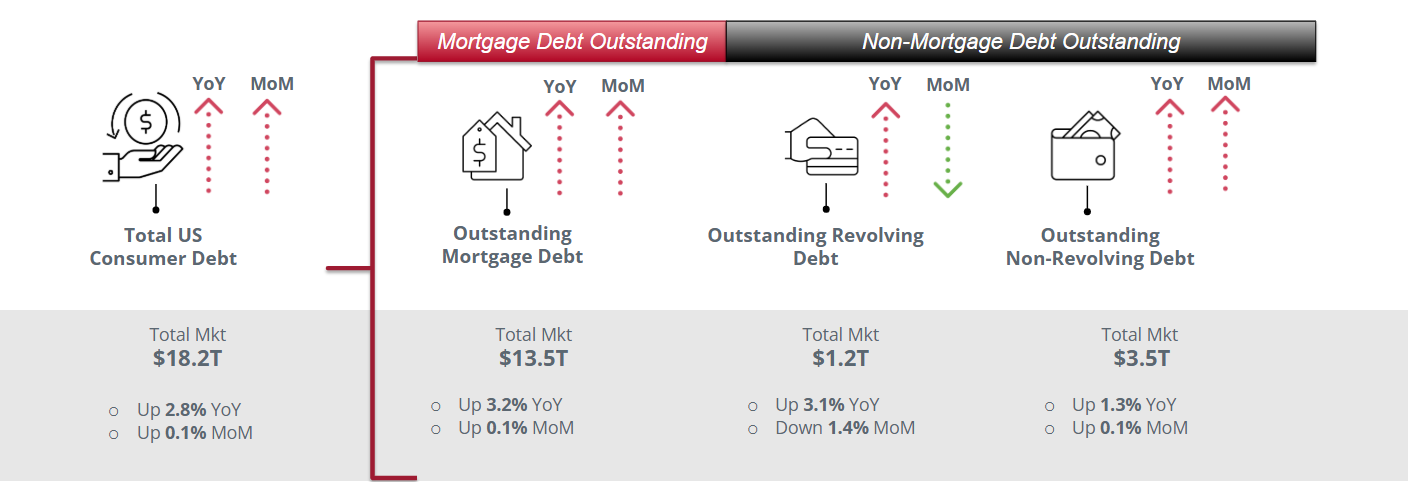

U.S. consumer debt reached $18.2 trillion due to strong year-over-year originations in auto, personal loans, bankcards, and mortgages, but a monthly contraction in revolving credit suggests households are actively managing day-to-day spending pressures.

-

Despite broad improvements in non-mortgage delinquencies, persistent housing affordability pressures are signaled by higher year-over-year mortgage delinquency, while small businesses are projected for a widespread recovery over the next year.

The May Market Pulse webinar showcased insights from Equifax Senior Advisor Jesse Hardin around current consumer credit trends.

May 2026 Key Insights: Today’s Consumer Credit Trends

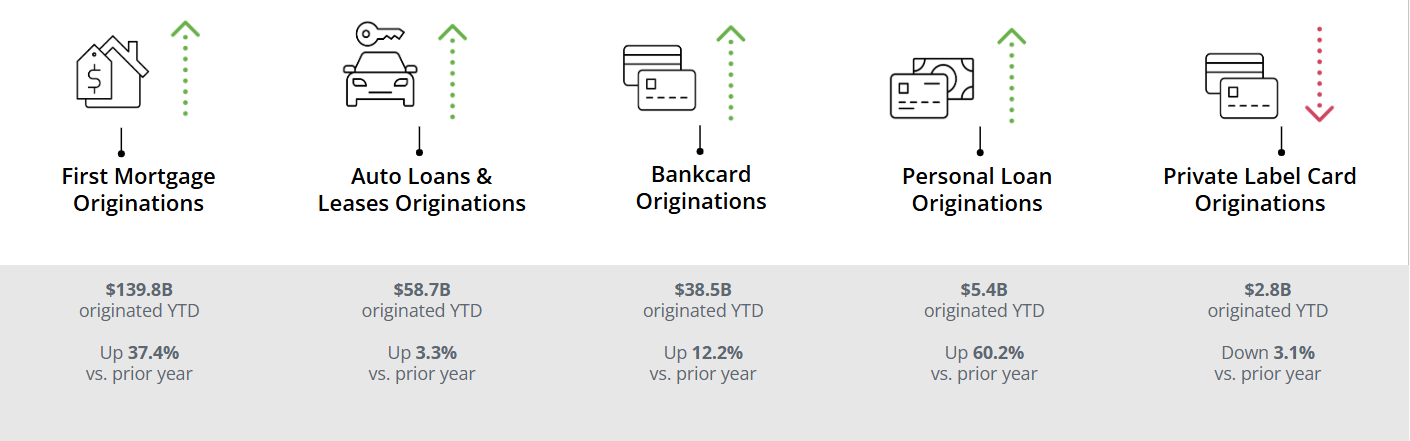

Sector-wide Expansion: Strong

year-over-year gains in auto, personal loans, bankcards, and

mortgages push overall credit originations higher.¹

Consumer Caution Emerges: Annual debt growth

pushes total U.S. consumer debt to $18.2 trillion, but a monthly

contraction in revolving credit suggests households might be

tightening their belts against economic pressures.² Mixed Debt Signals: While core auto and personal

lending continues to expand, the month-over-month contraction in

credit card usage points to consumers actively managing their

day-to-day spending pressures.²

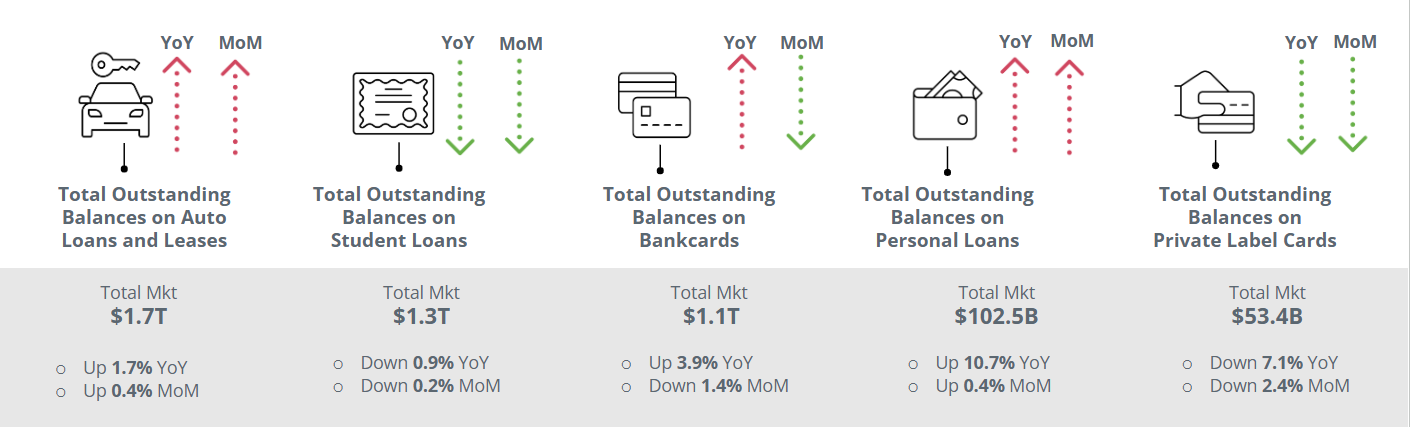

Mixed Debt Signals: While core auto and personal

lending continues to expand, the month-over-month contraction in

credit card usage points to consumers actively managing their

day-to-day spending pressures.²

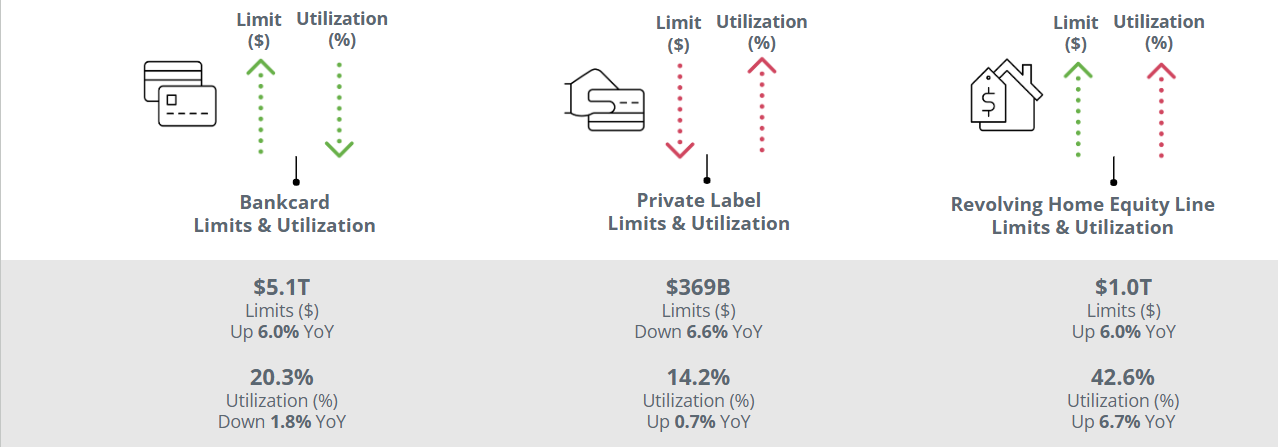

Credit Utilization Diverges: While general

bankcard usage cools despite higher limits, the growing reliance on

home equity lines suggests consumers are leveraging lower-cost,

asset-backed borrowing.²

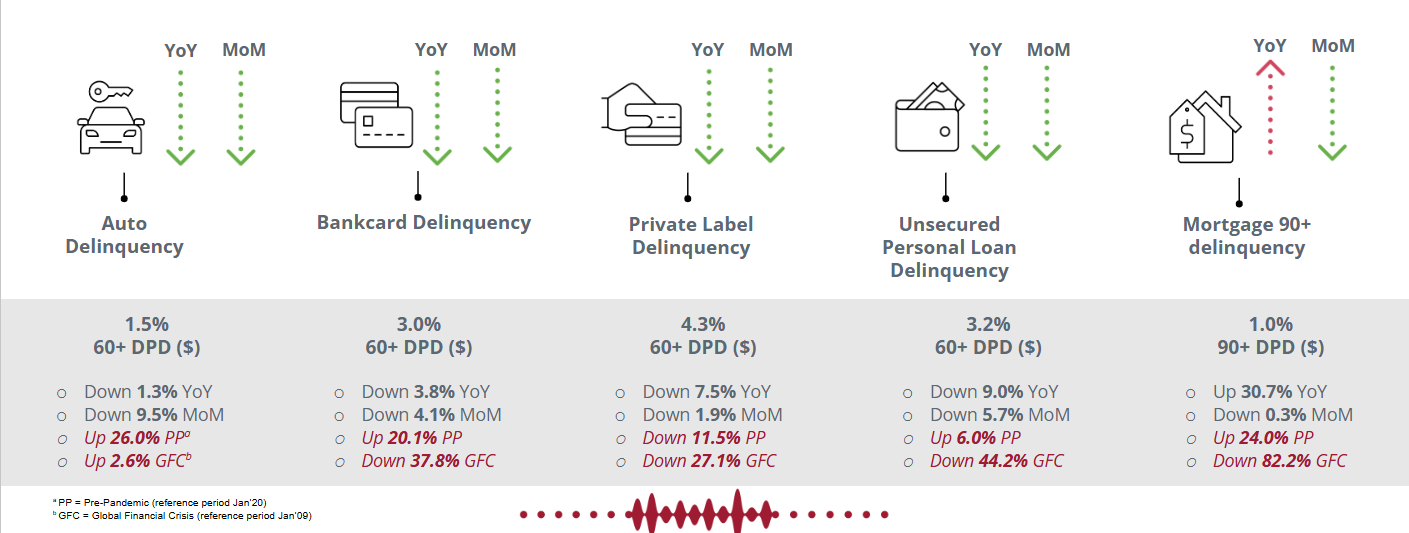

Mortgage Distress Continues: Broad improvements

in auto, card, and personal loan delinquencies contrast higher

year-over-year mortgage delinquency, signaling persistent housing

affordability pressures.²

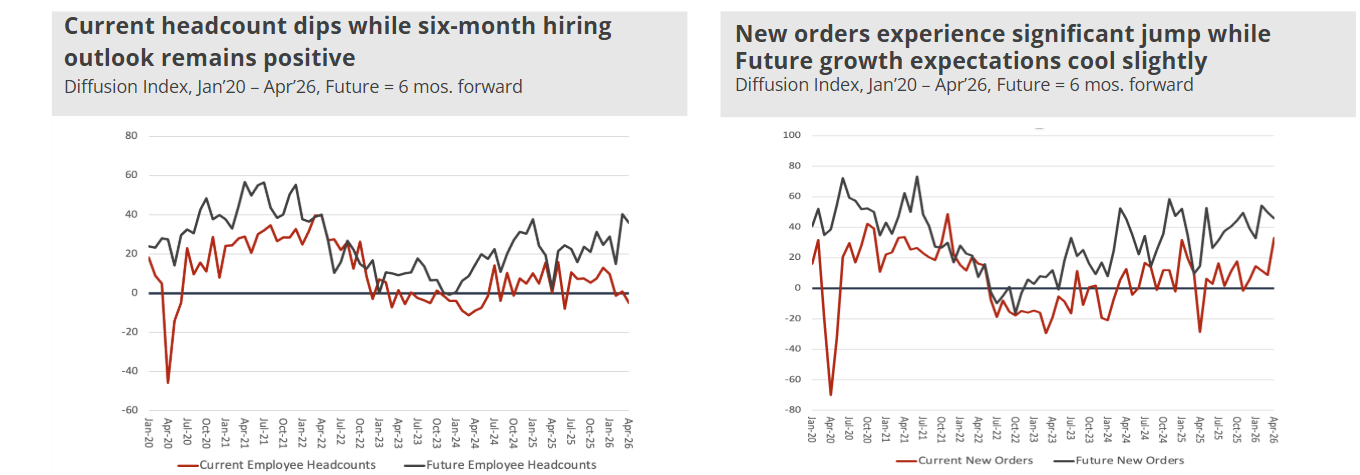

April Manufacturing Surge: Regional activity

and new orders expand, but firms experience overall decline in

employment and widespread input price increases.³

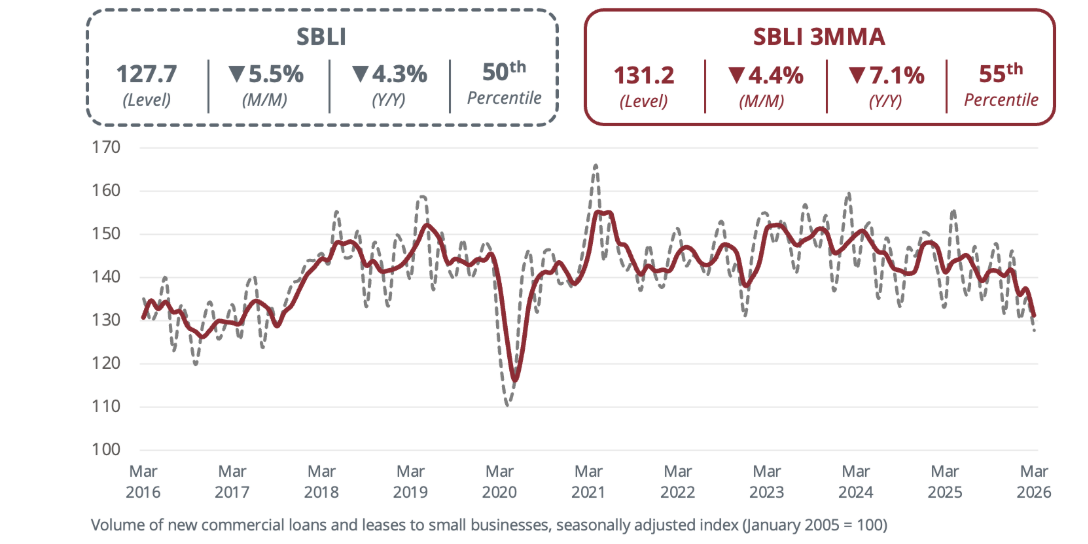

AI Buildout: AI is the backbone of business

investment growth, while small business lending and optimism have

softened in 2026.⁴

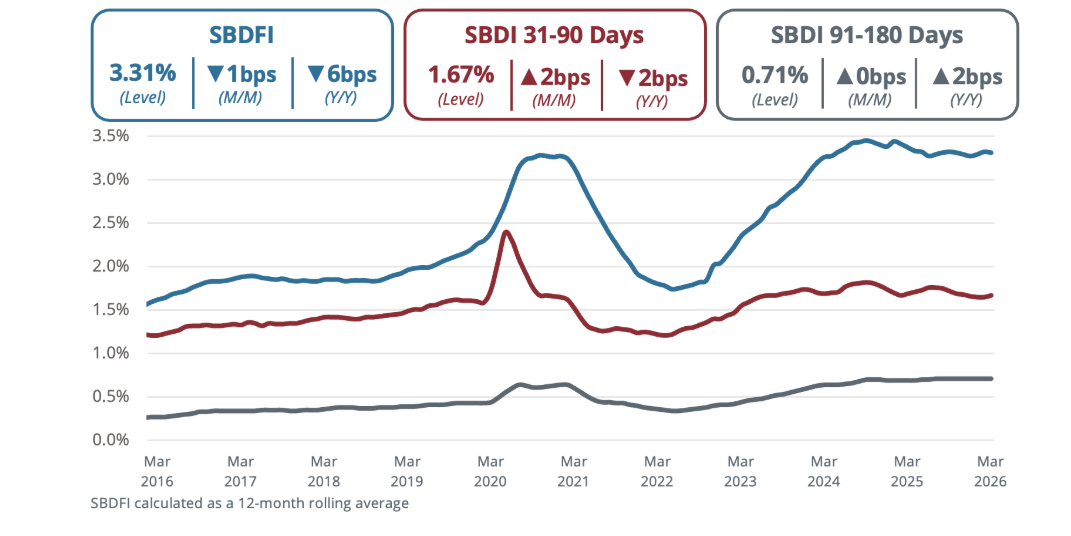

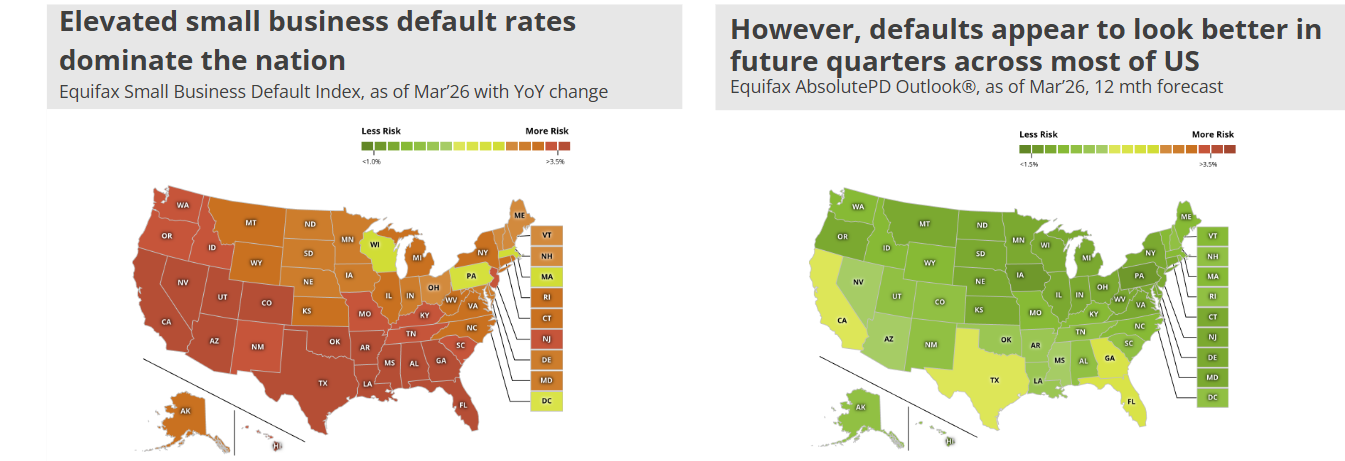

Optimism on Small Business Delinquency:

Delinquencies remain stable short-term moving only two bps lower in

five months, while longer-term delinquency flat for nine months.⁴

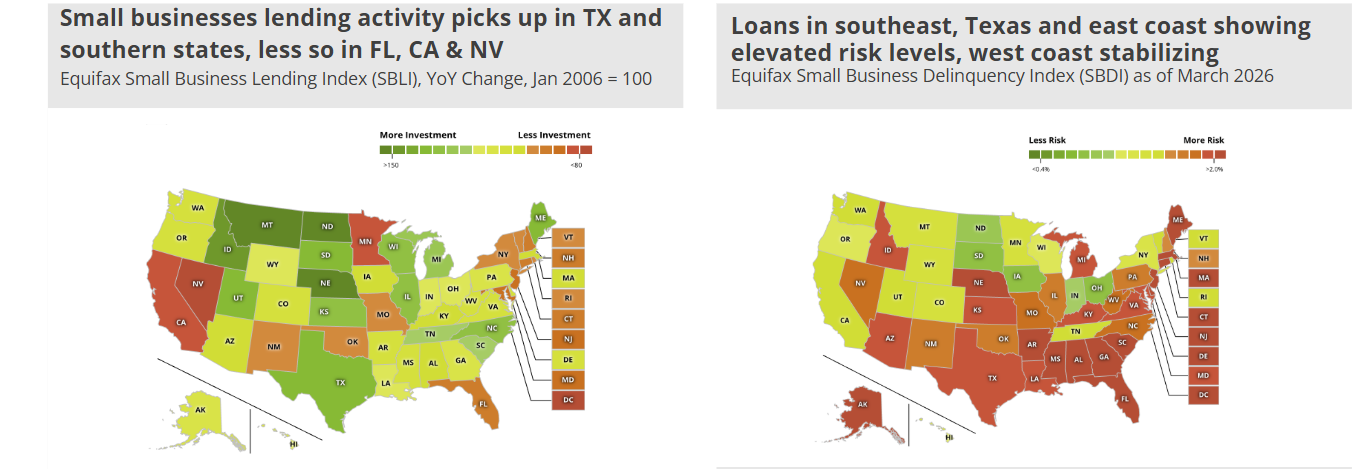

Small Business lending activity is hot in Texas

and some southern states, cooler out West, but hotter areas also show

increased risk potential.⁵

Forecast Brightens: The current sea of high

default risk is expected to clear, with widespread recovery projected

for small businesses over the next year.⁵

Keep Your Business Goals Within Sight

Find our monthly Small Business Insights, National Consumer Credit Trends reports, the Market Pulse podcast, and more at our Market Pulse hub.

Broaden your perspective with insights that inspire bold innovation, confident adaptation, and decisive leadership through Trend and Insights.

Sources:

-

Equifax US National Consumer Credit Trends Originations Report from April 2026 - Data through January2026

-

Equifax US National Consumer Credit Trends Portfolio Report from April 2026 - Data as of March 2026

-

Philadelphia Federal Reserve, Manufacturing Business Outlook Survey, April 2026

-

Equifax Main Street Lending Report from May 2026 - Data as of March 2026

-

Equifax Commercial Data, March 2026

(c) Equifax Inc. 2026. All Rights Reserved. The statistics provided herein are for informational and illustrative purposes only and shall not be used for any other purpose.

*The opinions, estimates, and forecasts presented herein are for general information use only. This material is based upon information that we consider to be reliable, but we do not represent that it is accurate or complete. No person should consider distribution of this material as making any representation or warranty with respect to such material and should not rely upon it as such. Equifax does not assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice. The opinions, estimates, forecasts, and other views published herein represent the views of the presenters as of the date indicated and do not necessarily represent the views of Equifax or its management.