The Tri-Merge Standard: Decades of Consistency and Risk Mitigation

Highlights:

-

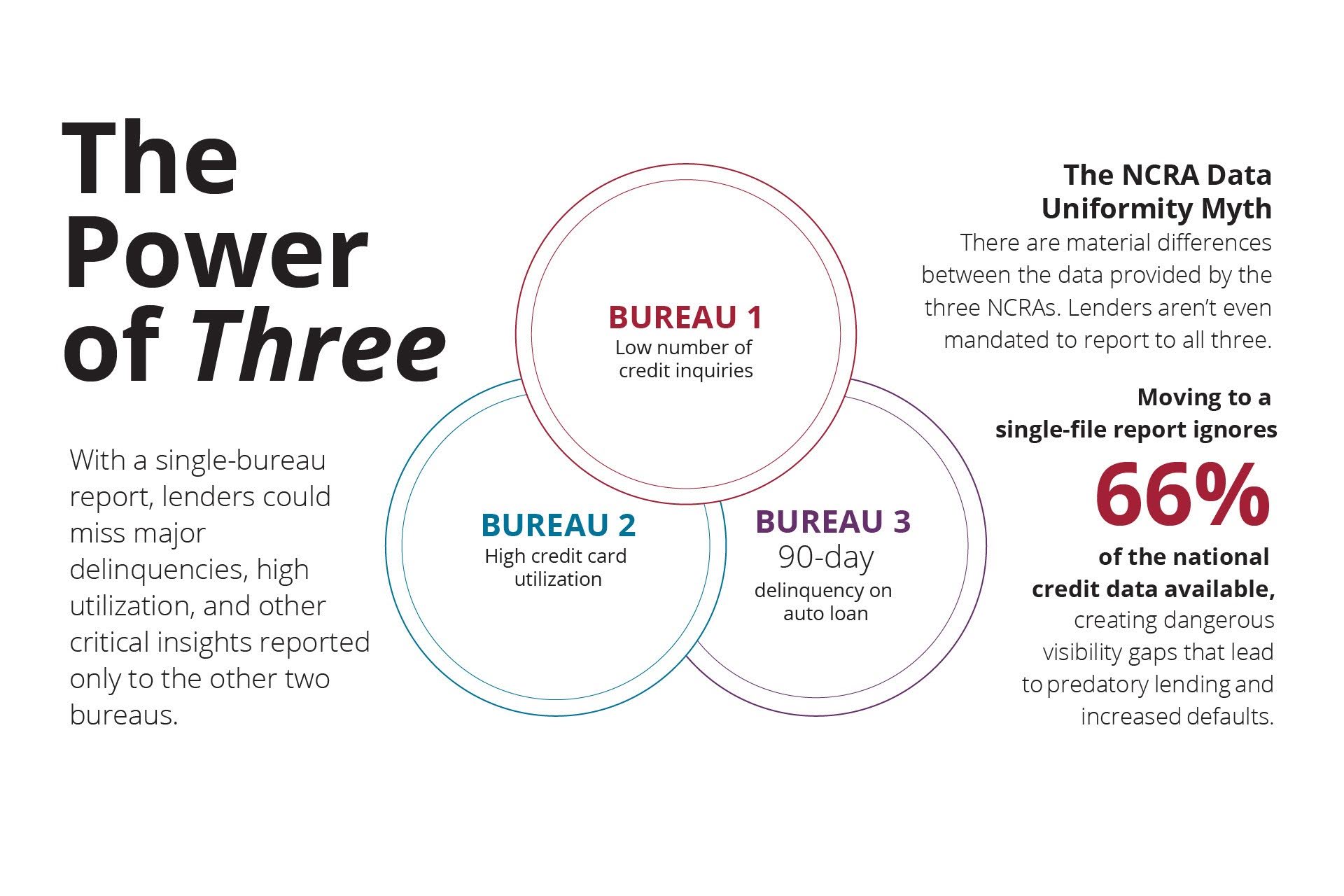

The Tri-Merge standard is essential for systemic risk mitigation in the mortgage market, as relying on a single bureau creates a "blind spot" and ignores 66% of available national credit data, significantly increasing the risk of defaults.

-

Combining comprehensive 3-bureau data with modern scoring models, like VantageScore 4.0, enables lenders to accurately assess risk, safely expand their "buy box," and qualify up to 10% more creditworthy borrowers.

In the complex landscape of the $13 trillion U.S. mortgage market, transparency and security are paramount to long-term stability. At the foundation of this security is the "Tri-Merge," a comprehensive credit report that integrates data from all three Nationwide Consumer Reporting Agencies (NCRAs) into a single, comprehensive protective barrier. Since becoming the industry standard in the 1990s, the Tri-Merge has consistently provided the most complete view of a borrower’s credit health, successfully protecting both lenders and consumers from hidden financial risks.

A History of Safety and Soundness

Prior to the 1990s, fragmented credit data frequently resulted in inconsistent lending decisions across mortgage originations. The Tri-Merge was established to solve this problem, ensuring that every lender had access to the exact same high-quality data needed to properly evaluate a 30-year financial commitment. Crucially, this system was specifically designed to shield the secondary market from systemic risk and ensure the safety and soundness of Government-Sponsored Enterprises (GSEs).

The Myth of Data Uniformity and the "66% Risk"

A growing misconception in the modern credit discourse is

that a single-bureau report is sufficient for risk assessment.

However, because lenders are not mandated to report data to all

three NCRAs, reporting remains purely voluntary. Consequently,

credit data is rarely uniform across the bureaus. Moving to a

single-file system introduces a massive "blind spot," as

it effectively ignores 66% of available national credit data. A

single-bureau pull might completely miss significant delinquencies

or high credit utilization that are only reported to the other two

bureaus, ultimately opening the door to predatory lending and

increased defaults. The industry itself recognizes this danger. In a recent National

Mortgage News (NMN) survey of 123 mortgage professionals, lenders

ranked comprehensive 3-bureau data as essential—not optional—for

avoiding hidden liabilities in origination. Furthermore, firms with

the highest annual originations emphasized that missing even a single

tradeline can significantly shift an applicant’s score band,

drastically altering their perceived risk.

The industry itself recognizes this danger. In a recent National

Mortgage News (NMN) survey of 123 mortgage professionals, lenders

ranked comprehensive 3-bureau data as essential—not optional—for

avoiding hidden liabilities in origination. Furthermore, firms with

the highest annual originations emphasized that missing even a single

tradeline can significantly shift an applicant’s score band,

drastically altering their perceived risk.

Debunking the "700+ Score" Shortcut

Some industry observers have argued that single-file reports can predict risk equally well for borrowers with credit scores over 700. This represents a significant analytical flaw, as their conclusion is based on loans that were already vetted through a full Tri-Merge. The "similar performance" observed in these 700+ score profiles is actually the direct result of the Tri-Merge process actively filtering out high-risk variables before the loan even closes. The hidden reality is that a 700+ score at one bureau can easily mask a 600-level reality at another due to reporting variations.

The High Stakes of Short-Term Cost-Cutting

It is a dangerous "race to the bottom" to compare the due diligence required for a 30-year mortgage to a standard 60-month auto loan. A mortgage demands the highest level of scrutiny. The NMN survey reinforces this priority, finding that when evaluating new credit scoring models, mortgage professionals rank the "accuracy of risk assessment" as the single most important factor. Reducing data transparency in pursuit of short-term savings inevitably increases loan delinquencies. If this lack of transparency leads to an erosion of credit quality within the Mortgage-Backed Securities (MBS) market, the taxpayer will ultimately bear the heavy cost of GSE volatility.

Protecting the Future of Homeownership

By providing a 360-degree view of borrower behavior, the Tri-Merge helps actively prevent the blind spots that lead to systemic risk and taxpayer-funded volatility. Legacy credit models often leave millions of creditworthy Americans in the dark. By pairing comprehensive 3-bureau data with modern scoring models, lenders can expand homeownership opportunities while keeping risk firmly in check. VantageScore 4.0 illuminates these consumers by utilizing a 24-month look back to assess the trajectory of a consumer's credit behavior, while also incorporating alternative data like rental history, telco, pay TV, and utility accounts that legacy models did not use. This visibility allows lenders to expand their "buy box" and uncover borrowers that legacy scores miss, helping to qualify 10% more borrowers, many of whom are first-time homebuyers.

The Tri-Merge is not just a reporting standard; it is the fundamental safeguard protecting the overall safety, soundness, and long-term stability of the American mortgage market.