Small Business Lending Increased in December 2025

THE EQUIFAX December SMALL BUSINESS LENDING INDEX (SBLI) showed that nominal small business lending volumes increased 10.4% month-over-month (but decreased 3.5% year-over-year). The SBLI three-month moving average increased 0.6% month-over-month but decreased 4.1% year-over-year.

Meanwhile, the Equifax Small Business Delinquency Index (SBDI) 31-90 Days Past Due was 1.66% in December, down two basis points month-over-month and down eight basis points from December 2024. The SBDI 91–180 days past due remained level at 0.71% from November 2025 to December 2025. The Small Business Default Index (SBDFI) measured 3.19% and was down six basis points month-over-month.

The month-over-month improvement of the SBLI was paired with continued stability in small business credit quality: short term (31–90 days) and severe (91–180) delinquencies were flat in December, while defaults fell six basis points.

Small business economic optimism held steady around the historical average leading into 2026, largely driven by expectations for greater revenue and profit growth in the new year. However, hard economic data (as opposed to soft, sentiment-focused data) show a slight dip in small business financials at the close of 2025. Looking ahead, the outlook is mixed, but the possibility of a more dovish posture from the Federal Reserve this year could provide a boost to small business lending and expansion plans.

Regional Analysis

Small Business Lending:

In December, only 20 states had a year-over-year increase in 12-month rolling lending volumes. Of the 10 largest* states, five showed an increase from 2024. Georgia had the strongest improvement at 5.4%. California decreased the most at -9.1%. Of all states, Oklahoma (+13%) and Wyoming (+11%) had the highest growth numbers compared to the same period last year. Alaska (-19%) and South Dakota (-11%) posted the largest decreases from December 2024 of all states.

Month-over-month, nominal lending activity was down in 32 states in the preceding 12 months, including six of the 10 largest states. Most of the remaining states where lending increased showed increases of less than 1%: only Pennsylvania increased by a measurable margin, up 2.6%. Of all states, Alaska (-6% month-over-month) and South Dakota (-6% month-over-month) decreased the most. Of 50 measured states, only 10 had month-over-month increases over 1%, led by Oklahoma (+5%).

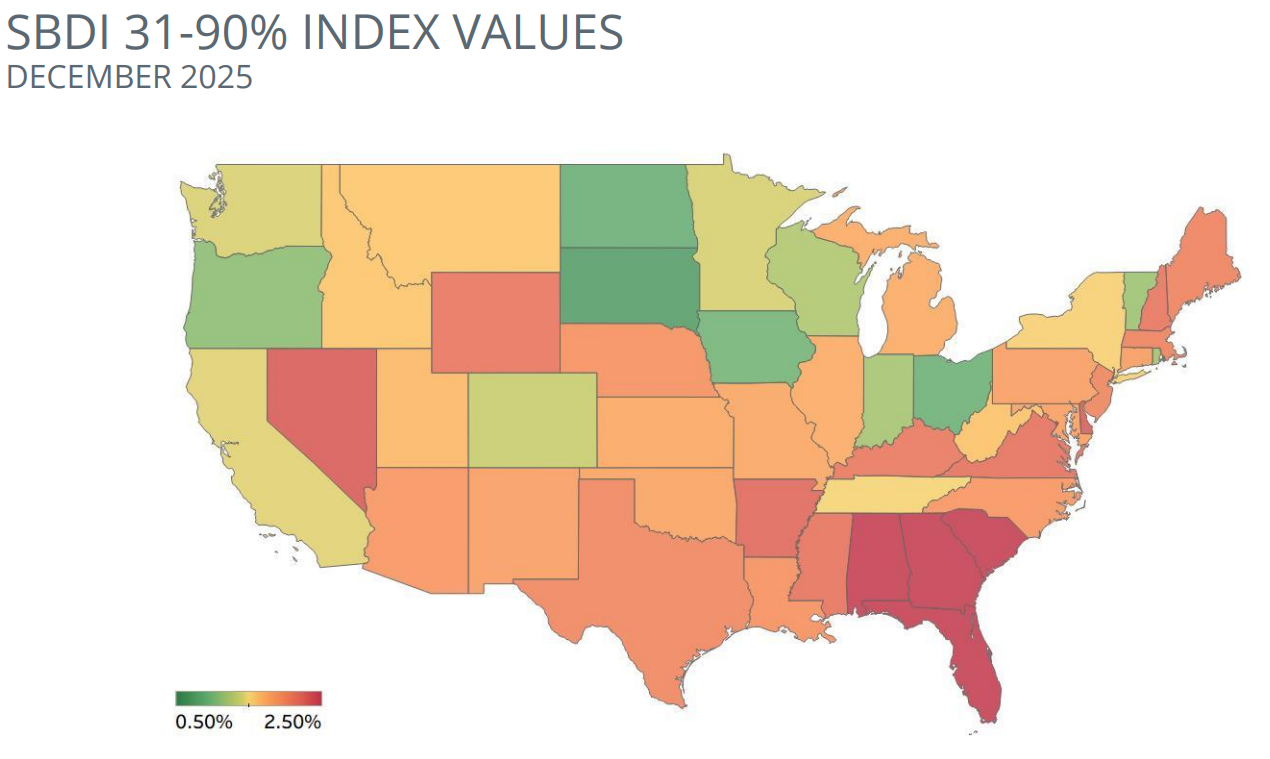

Small Business Delinquency and Default:

Defaults decreased in 39 states year-over-year and decreased in 45 states month-over-month. Year-over-year, Massachusetts improved the most, declining by 33%, while Colorado had the largest default rate increase, jumping 14%. Florida (4.5%), Texas (4.4%), and Georgia (4.1%) had the highest overall default rates among all states. North Dakota (1.9%) and Massachusetts (2.1%) had the lowest. Of the 10 largest states, only Texas and Georgia increased default rates in December 2025, rising 2.7% and 2.4% year-over-year, respectively. The remaining states decreased default rates year-over-year, led by New York which dropped by 27%.

In 31-90 day delinquency, 33 states had an increase in delinquency month-over-month. Florida (2.9%), Georgia (2.7%), and Alabama (2.7%) had the highest delinquency rates in December 2025, while South Dakota (0.7%), North Dakota (0.9%), and Ohio (0.9%) had the lowest. Delaware showed the largest year-over-year increase in delinquency, rising 110 basis points since last December. Of the 10 largest states, Michigan (+41 basis points) and Illinois (+10 basis points) had the largest year-over-year increases. California decreased 28 basis points from December 2024, and New York dropped 21 basis points.

Industry Analysis

Small Business Lending:

-

In December 2025, nominal small business lending fell in five of the 17 tracked industries month-over-month, holding steady in eight industries including Wholesale Trade, Manufacturing and Construction.

-

12-month rolling lending activity weakened most month-over-month (-3%) in both Information and Agriculture, Forestry, Fishing and Hunting.

-

Compared to December 2024, lending rose the most in Finance and Insurance (+4%) followed by Art, Entertainment, and Recreation (+3%) and Real Estate and Rental Leasing (+3%). Lending fell in Information (-14%), followed by Mining, Quarrying, and Oil and Gas Extraction (-6%), Accommodation and Food Services (-6%), and Transportation and Warehousing (-6%).

Small Business Delinquency and Default:

-

In December 2025, the annualized SBDFI rose or held steady month-over-month in five of the 17 tracked industries, with the largest increase in Agriculture, Forestry, Fishing and Hunting (+4%).

-

From December 2024 to December 2025, the SBDFI increased in seven of the 17 tracked industries, led by Mining, Quarrying, and Oil and Gas Extraction (+11%) and Agriculture, Forestry, Fishing and Hunting (+8%).

-

From December 2024 to December 2025, the 31-90 day SBDI increased 10% in the Agriculture industry and 1% in Construction. All other segments improved, with Transportation dropping 8% and General decreasing 7%.

Produced monthly, the Small Business Indices help lenders and businesses track changes in the small business marketplace by providing insights into lending, default and delinquency trends. To learn more and view the latest reports, check out our Small Business Indices page.

*By population