Conquer K-Shaped Consumer Risk: 5 Questions to Answer to Unmask Decision Intelligence Blind Spots

Highlights:

-

Equifax Risk Decision Intelligence empowers lenders to leverage traditional credit scores by layering FCRA-compliant alternative data, identity confidence metrics, and capacity precision insights to identify creditworthy borrowers.

-

By adopting a modular framework that integrates real-time behavioral insights, financial institutions can proactively manage portfolio risk, minimize default exposure, and safely maximize loan growth in a fluctuating economy.

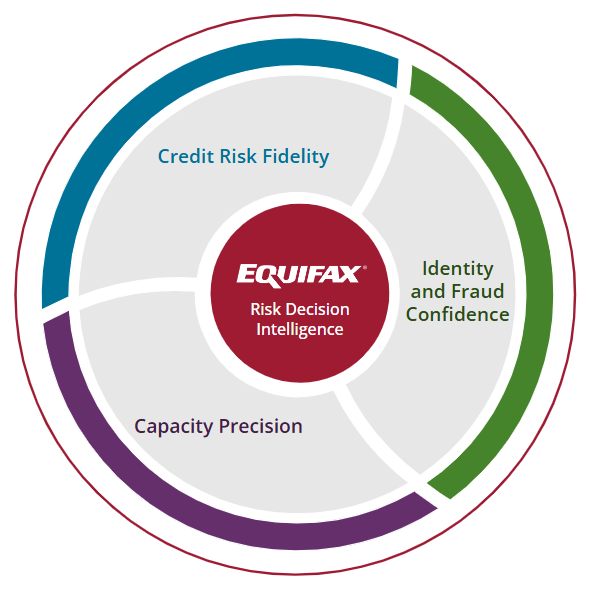

While some economic measures point to market resilience, these aggregate metrics mask a critical structural shift: we are operating in a K-shaped economy where the middle class is shrinking, trading down, and drawing down savings. To help lenders navigate this fragmentation, Equifax developed Risk Decision Intelligence, a strategic framework that layers FCRA-compliant alternative data and real-time insights directly over the traditional credit file. Traditional credit scores remain the vital foundation of risk assessment. They offer an essential baseline of historical creditworthiness. However, relying solely on them creates a consumer risk blind spot.

To see if your institution is protected, ask yourself these 5

critical questions across the three pillars of Equifax Risk Decision Intelligence:

Pillar 1: Credit Risk Fidelity (Do we have the full picture of a consumer’s payment history?)

Q: Are we unintentionally saying no to creditworthy borrowers who lack traditional history?

Leaning exclusively on traditional credit files locks you out of 76.1 million credit-invisible or thin-file U.S. consumers. By upgrading to VantageScore®, which integrates trended data, and layering alternative data assets like utility and telecom history, you can reduce your unscorable population by 32% and safely approve more applicants.

Pillar 2: Identity and Fraud Confidence (Is the applicant real, and do they intend to pay?)

Q: Can we distinguish between a borrower's ability to pay and their intent to defraud?

Traditional scores measure a consumer's past ability to pay, but they do not flag a bad actor's immediate intent to default. Synthetic identity fraud alone drives up to 15% of charge-offs, yet traditional methods miss 95% of it. Layering specialized behavioral metrics like Credit Abuse Risk scoring alongside your core foundation yields a 67% increase in captures of the riskiest 1% of accounts.

Pillar 3: Capacity Precision (How much can they truly afford to borrow without defaulting?)

Q: Do we accurately understand a borrower's true debt capacity and financial limits?

With severe delinquencies showing upward pressure in key secured sectors like mortgages, understanding a customer's true capacity has become business-critical. Relying exclusively on static scoring models fails to define a safe lending limit, meaning even a traditionally good customer can be pushed past their financial threshold. Gaining advanced, layered insight into how much debt a customer can safely handle allows you to set precise limits, protecting your portfolio from over-lending losses while identifying opportunities to safely maximize loan amounts.

Q: Are we actively monitoring real-time behavioral shifts before delinquency hits?

Traditional credit scores are backward-looking by design. To protect your portfolio, you must monitor real-time shifts in payment velocity—such as tracking consumers who drop from paying credit card balances in full to only paying the monthly minimum—to manage limits proactively.

Holistic Workflow Integration

Q: Is our core foundation optimized to give us advanced insight without adding extra cost?

Industry adoption of VantageScore® is surging because it delivers deep, forward-looking insights engineered for today's market complexity. In many cases, you can switch to VantageScore® as your core foundation to unlock these advanced capabilities at a better value, or even with zero additional expenditure, providing the perfect integration baseline

Stop Guessing. Start Seeing.

The line between a profitable account and a preventable default has never been thinner. Equifax Risk Decision Intelligence is a modular, scalable framework designed to seamlessly supercharge your existing underwriting workflows without rebuilding from scratch.

More Insights. Superior Outcomes. Less Cost. That is the promise of true intelligence.

Ready to eliminate the blind spots in your portfolio?

Schedule your personalized meeting and sign up for a custom validation and pilot that will transform your underwriting. Don't delay, your competitive advantage starts now.