November 2025 Consumer Pulse: The Latest Consumer Credit Trends

Highlights:

-

Consumer originations have increased year-over-year across most lending categories through July 2025 (excluding private label cards). Outstanding mortgage and revolving consumer debt continue to climb, leading to the insight that lenders should prepare for increased demand for credit cards and loans during the 2025 holiday season.

-

As of September 2025, auto and mortgage delinquencies rose year-over-year but remained below pre-pandemic levels. In contrast, delinquencies for bankcard, private label, and personal loans improved year-over-year, and student loan delinquency continues to decline.

The November Market Pulse webinar showcased insights from Equifax Senior Advisor Maria Urtubey around current consumer credit trends. While this overview is meant to be a snapshot of the larger discussion, you can receive full access to the standard charts and graphs by reaching out to the Equifax Advisory team: RiskAdvisors@Equifax.com.

November 2025 Key Insights: Today’s Consumer Credit Trends

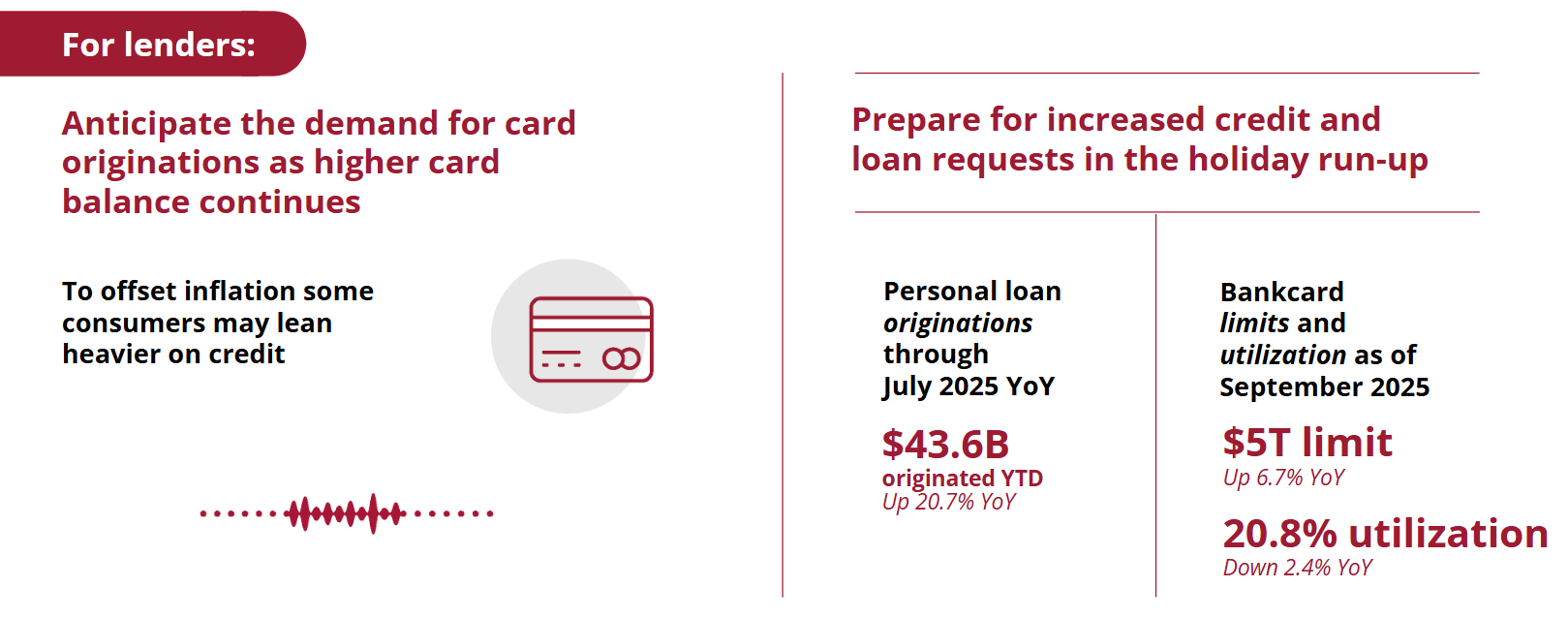

Through July 2025, consumer originations rose year-over-year

across all lending categories, but private label card was lower

year-over-year.¹

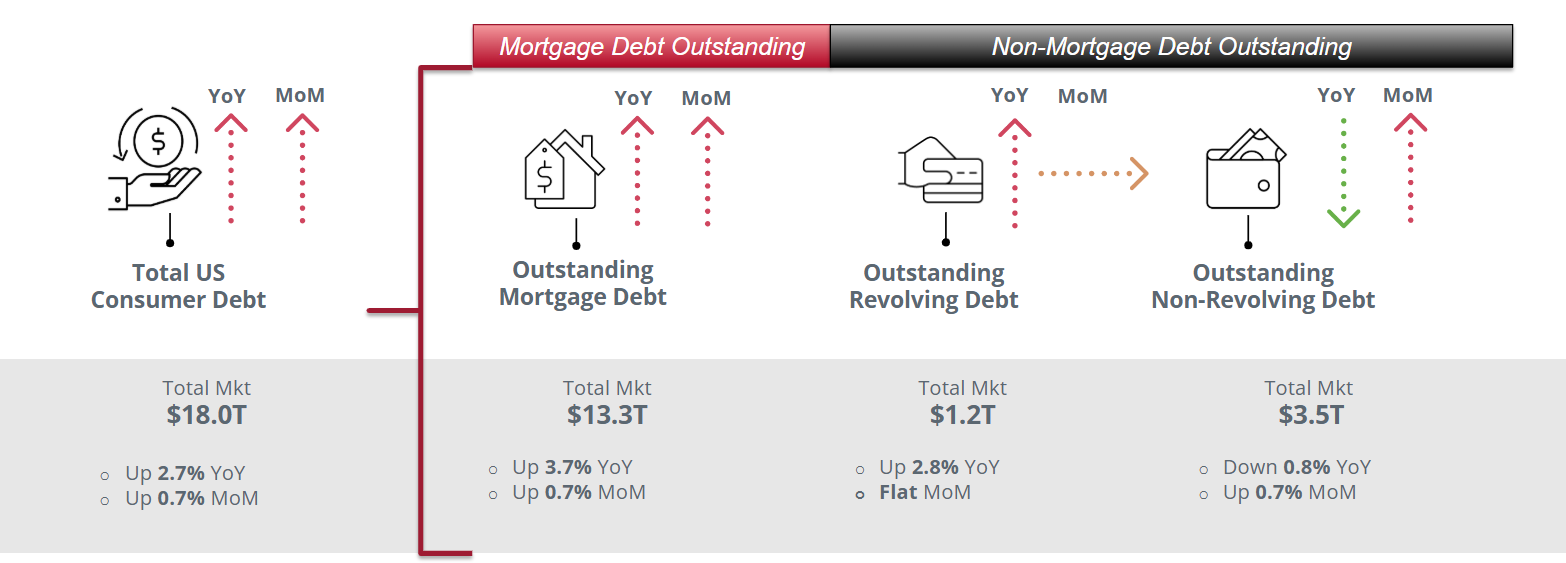

As of September 2025, outstanding mortgage, including first

mortgages, HELOCs, and HELOANs, and revolving consumer debt, including

bankcard, private label cards, and other revolving products, continue

to climb year-over-year, while non-revolving, including auto loans and

leases, students loans, and personal loans, has slowed year-over-year,

but rose month-over-month.²

As of September 2025, non-mortgage consumer debt outstanding

has increased for auto, bankcards and personal loans year-over-year.

Student loans and private label cards continue to be lower.²

What does the data tell us for the 2025 holiday

season?³ Lenders should prepare for increased demand for credit

cards and loans.

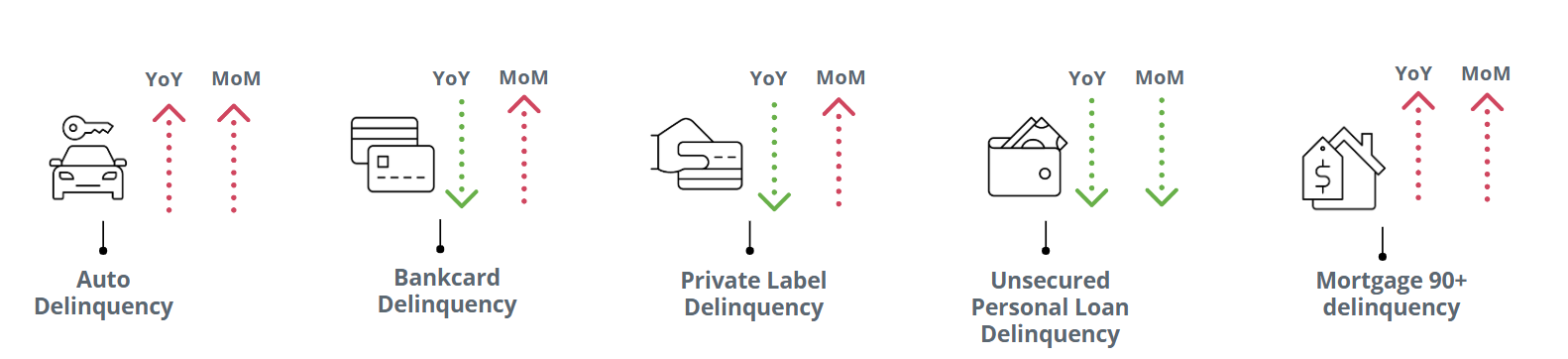

September 2025 auto and mortgage delinquencies increased

year-over-year, while unit and debt delinquencies continue to stay

below pre-pandemic levels. Bankcard, private label and personal loans

improved year-over-year.²

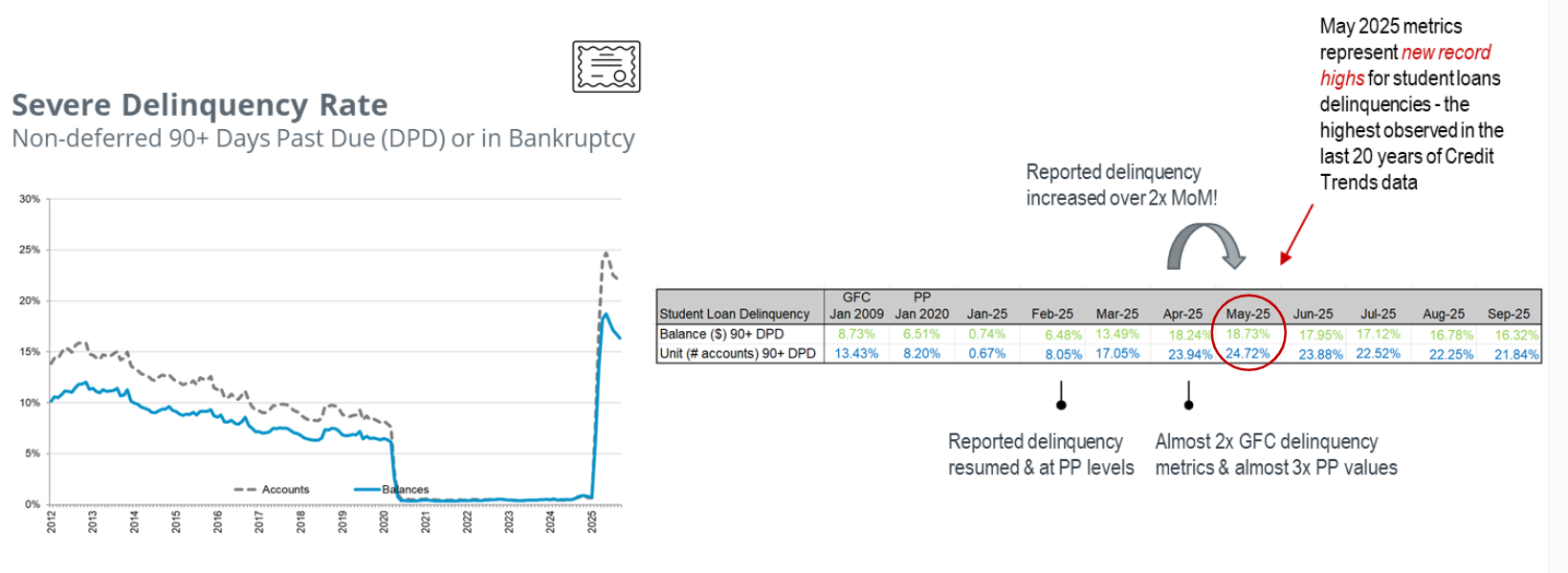

Student loan delinquency continues to decline in September

after historic peak observed in May 2025.²

Keep Your Business Goals Within Sight

We hope you will join us for our December 2025 Market Pulse webinar taking place on Thursday, December 4, 2025, where our talented and dynamic panel will discuss how AI could shape 2026 and beyond. To ask questions in real time and gain deeper insights before anyone else, you must be there. Don’t miss it!

Find our monthly Small Business Insights, National Consumer Credit Trends reports, the Market Pulse podcast, and more at our Market Pulse hub.

Broaden your perspective with insights that inspire bold innovation, confident adaptation, and decisive leadership through Trend and Insights.

Sources:

-

Equifax US National Consumer Credit Trends Originations and Portfolio Reports from October 2025

(c) Equifax Inc. 2025. All Rights Reserved. The statistics provided herein are for informational and illustrative purposes only and shall not be used for any other purpose.

*The opinions, estimates, and forecasts presented herein are for general information use only. This material is based upon information that we consider to be reliable, but we do not represent that it is accurate or complete. No person should consider distribution of this material as making any representation or warranty with respect to such material and should not rely upon it as such. Equifax does not assume any liability for any loss that may result from the reliance by any person upon any such information or opinions. Such information and opinions are subject to change without notice. The opinions, estimates, forecasts, and other views published herein represent the views of the presenters as of the date indicated and do not necessarily represent the views of Equifax or its management.