Undisclosed Debt Monitoring™ (UDM)

Clear to Close: Avoid "Surprises" at Loan Closing Due to Undisclosed Debt

During mortgage processing, there’s a vulnerable blind spot for lenders—the quiet period between the initial credit pull and the final loan closing, when borrowers will sometimes open new credit lines or loans that can alter their debt-to-income (DTI) ratio. Even small shifts in DTI can unravel a loan package at closing or lead to costly repurchase demands.

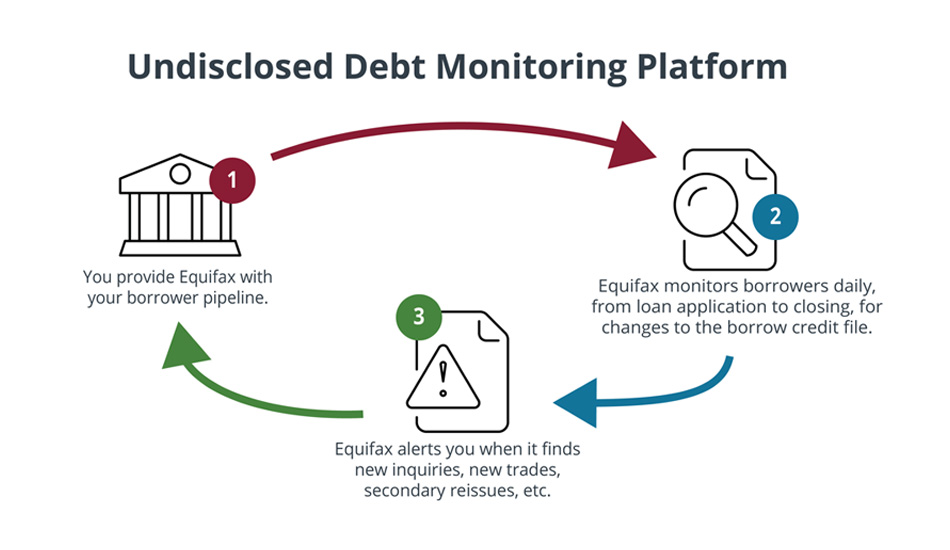

Instead of being blindsided by new, undisclosed loan activity at closing, lenders can use Undisclosed Debt Monitoring™ (UDM) to automatically monitor borrower credit activity during the quiet period and alert them whenever new activity is detected, so they can work with borrowers to proactively address changes prior to closing.

With UDM, lenders can confidently close more loans faster and with fewer complications and delays, and less risk.

10% of consumers opened other loans during the mortgage origination process.

36% of borrowers who opened only one new tradeline during the quiet period increased their DTI ratio by at least 3%.

46% of consumers pulled other credit inquiries before their mortgage loan closed.

*Equifax data analysis

Optimize Mortgage Loan Closing, Industry Confidence, and Borrower Experiences with Fewer Issues

In today's fast-moving economic environment, mortgage lenders need continuous visibility into day-to-day borrower credit activity throughout mortgage processing to better avoid unexpected closing issues that can wreck loan approvals, drive up lending costs, and lead to increased loan buyback demands.

UDM delivers the 24/7 visibility lenders need regarding new borrower credit inquiries, accounts, and loans initiated after the initial credit pull, during the quiet period of loan origination.

This helps borrowers, lenders, and lending partners confidently get to closing, faster, with fewer bottlenecks and less risk.

Promote Industry Best Practices

Integrate an automated tool that reduces blind spots in mortgage lending, while improving loan quality and borrower experiences.

Quickly Recalculate DTI

Based on the latest credit activity alerts, review and recalculate DTI as needed for individual borrowers to ensure loan closing remains on track.

Automated Credit Updates and Alerts, Delivered 24/7

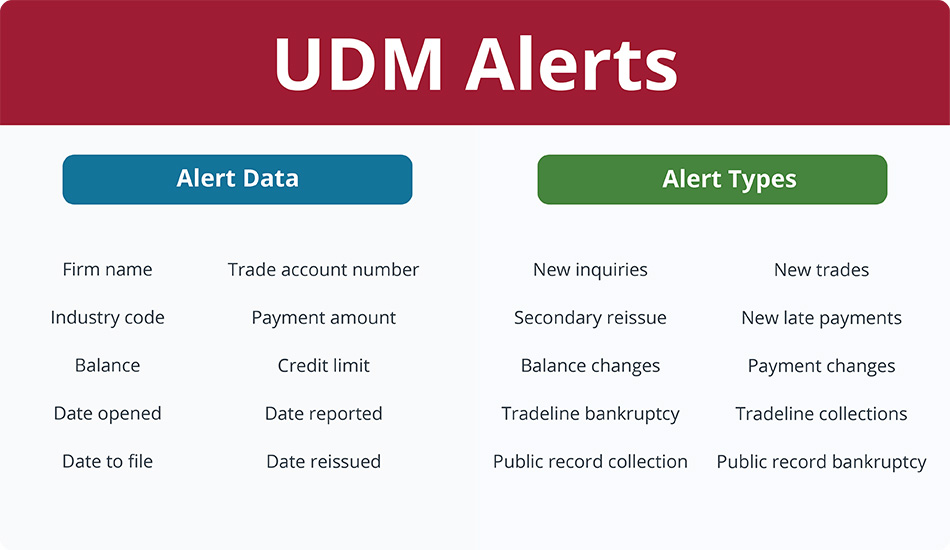

UDM monitors credit activity around the clock, 24/7/365. If a new inquiry, tradeline, or other credit change is identified, the lender receives a variety of alerts for further investigation.

- 24/7 Monitoring continuously reviews loan files in your pipeline for new tradelines and other changes

- Daily alerts are triggered anytime relevant new activity is discovered

- Automated Integration supports use as a standalone digital service or integrated directly into a lender's technology platform (LOS)

- Dual bureau monitoring available

- Quarterly alert reports available for performance assessment

- Monitor for up to 180 days versus 120 days

- No max or limit on the number of alerts

- Option to connect via API

Protect Loan Closing by Monitoring for Undisclosed Debt Throughout Mortgage Processing

Avoid last-minute closing surprises with robust, integrated alerts tailored to your unique mortgage lending strategy and technology system.

UDM monitors borrower credit from application throughout the quiet period of mortgage underwriting and origination, alerting mortgage lenders to new, undisclosed debt early—before it disrupts loan closing.

Enroll now and start getting loan-saving alerts within 24 hours of newly detected credit activity.

- Improve borrower visibility with fewer blind spots

- Offer better borrower experiences

- Reduce repurchase demands, loan fallout, and related expenses that drive up lending costs

Frequently Asked Questions

Related Resources

Related Products

Mortgage Merged Credit Report Plus

Our Mortgage Merged Credit Report Plus provides traditional data from all three major credit reporting agencies along with differentiated, highly structured telco, pay tv and utilities attributes.